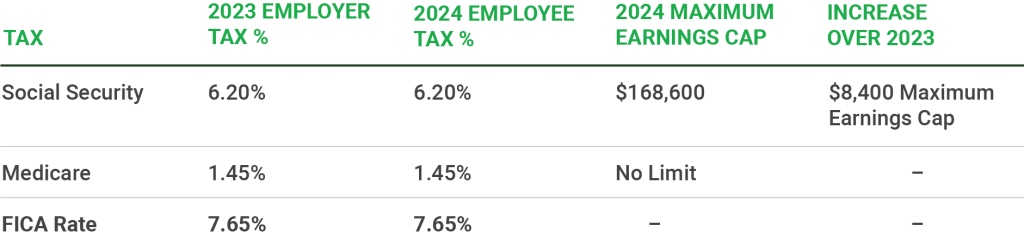

The construction industry plays a role in shaping our physical environment, careers in managing, designing, construction, maintenance of buildings, infrastructure, and various civil engineering projects. It is a multifaceted industry that spans residential, commercial, industrial, and public works projects. With continuous technological advancements and changing regulations in the construction industry, it is important for HR professionals to accurately benchmark salaries based on current market data.

Salaries in the Construction Industry

Compensation in the construction industry can vary widely based on myriad factors, including location, project size, company size, and experience. Understanding top construction CEO salaries provides valuable insights into market dynamics and the competitive landscape and is an important part of executive compensation planning. For more in-depth analysis, use ERI’s Executive Compensation Assessor to benchmark executive compensation packages for planning and reporting. For instance, see how construction management salaries vary by geographic location and company size. You can review current data for executive salaries, bonuses, non-equity incentives, stock awards, option awards, pension, and other compensation to help benchmark total executive compensation and ensure executive compensation packages remain competitive.

Top 10 Highest-Paid CEOs in the Construction Industry

For the purposes of this examination, base salary serves as the metric since it is predetermined and the most fixed among the various forms of executive compensation. Other pay, defined as excess benefits and perquisites greater than $10,000, is the second most common form of CEO compensation and is also included in the table below.

The following is a summary of top CEO pay in the construction industry. Industries are defined using the Standard Industrial Classification (SIC) system as indicated by the organization. This summary covers organizations that filed in any SIC from 1500 to 1799.

| Company | Name | Title | Salary | Other Pay |

| D.R. Horton Inc | David Auld | President and Chief Executive Officer | $700,000 | $29,296,862 |

| NVR Inc | Eugene Bredow | President and Chief Executive Officer | $715,204 | $18,573,806 |

| KB Home | Jeffrey Mezger | Chairman of the Board, President, and Chief Executive Officer | $1,150,000 | $14,664,791 |

| M.D.C. Holdings Inc | David Mandarich | Director, President, and Chief Executive Officer | $1,000,000 | $14,683,346 |

| Jacobs Engineering Group Inc | Steven Demetriou | Chairman of the Board and Chief Executive Officer | $1,411,154 | $13,204,367 |

| PulteGroup Inc | Ryan Marshall | Director, President, and Chief Executive Officer | $1,000,000 | $13,484,024 |

| Otis Worldwide Corp | Judith Marks | Chairman of the Board, President, and Chief Executive Officer | $1,300,000 | $13,177,875 |

| KBR Inc | Stuart Bradie | Director, President, and Chief Executive Officer | $1,191,360 | $11,425,675 |

| Quanta Services Inc | Earl Austin | Director, President, and Chief Executive Officer | $1,225,342 | $10,813,618 |

| Carlisle Companies Inc | D. Koch | Chairman of the Board, President, and Chief Executive Officer | $1,330,000 | $10,187,926 |

Building total compensation packages for top executive employees can vary considerably across organizations due to a variety of complex factors. Use ERI’s Executive Compensation Assessor to learn more about how construction executive salaries compare to those in other industries, considering total compensation factors such as salary, stock, incentives, bonuses, and more. Keep in mind that compensation figures may change over time, reflecting market dynamics, company performance, and industry trends. Always stay informed of the latest compensation data to ensure your salary planning remains up to date and competitive within your industry.

Learn more about top 10 executive compensation in various industries at ERI, including the top 10 highest-paid medical professionals in nonprofit health care and the top 10 highest-paid CEOs in technology.