In a tight labor market, it is increasingly important for organizations to offer competitive benefits packages in order to attract, retain, and motivate employees. Whereas very small businesses might only offer basic benefits with few options, larger organizations often enhance their total compensation packages by providing an array of robust benefits offerings tailored to the needs of their employees. Given the seemingly endless options available, HR and compensation professionals need to have current market data on trends in employee benefits that reflect their organizations’ specific geographic region, industry sector, and organization size.

The Value of Offering Employee Benefits

Offering attractive employee benefits will improve the total compensation package that you use to attract new employees, giving you an advantage in a competitive labor market in which organizations are striving to win over top talent. For existing employees, offering a well-rounded benefits package with an array of options that are valuable and meaningful to employees will lower employee turnover, lead to increased retention, and even motivate employees.

What Is a Benefits Package?

A comprehensive employee benefits package may include these offerings: health and wellness benefits, financial and retirement benefits, time-off and leave benefits, and mandatory benefits, plus an array of possible additional benefits.

Types of Employee Benefits

Health and wellness benefits often include the following:

- Medical Insurance

- Dental Insurance

- Vision Insurance

- Life Insurance

- Disability Insurance

- Employee Assistance Program

Financial and retirement benefits may include these options:

- Pension Plan

- 401(k) Plan

- 403(b) Plan

- 457 Plan

- SEP-IRA Plan

- Roth 401(k) Plan

- Money Purchase Plan

Time-off and leave benefits often include the following:

- Paid Time Off

- Paid Holiday Time

- Paid Sick Time

- Paid Bereavement Time

In the United States, these four categories encompass federally mandatory employee benefits:

- Government Health Care

- Government Retirement

- Federal Unemployment

- Workers’ Compensation

How to Build a Competitive Employee Benefits Package

In order to design an effective employee benefits package that fits your budget and is competitive in your local labor market, you will need to follow several steps:

Step 1: Create a Plan Listing Mandated and Voluntary Employee Benefits

First, create an initial plan for required and optional employee benefits that your organization is interested in exploring.

Mandated Employee Benefits

In the United States, there are several federally mandated benefits that employers are required to provide to their employees to ensure basic medical care, retirement income, essential income in the event of loss of work or a disability, and liability coverage for workplace-related injuries and illness. Unlike voluntary employee benefits, these are legally required. According to the Bureau of Labor Statistics (BLS), federally mandated employee benefits accounted for 7.2% of total compensation and 23.2% of total benefits in September 2022, so these benefits should be factored carefully into any organization’s budget.1

The Employer Cost for Employee Compensation (ECEC) survey conducted by the BLS provides useful data for these four categories of federally mandated employee benefits:1

- Medicare – This federal benefit pays medical care for retirees and individuals with long-term disabilities.

- Social Security– Enacted in 1935, Social Security benefits provide basic income for retired workers, dependents, and disabled workers, along with their families.

- Federal Unemployment Insurance– Alongside state unemployment insurance programs, federal unemployment insurance provides income payments to eligible workers who have been laid off from their jobs.

- Workers’ Compensation– This federal benefit pays for medical expenses and provides for lost income as a result of work-related injuries and illnesses.

Voluntary Employee Benefits

Organizations have an array of options to consider when selecting voluntary employee benefits to include in their overall benefits packages. While optional, as opposed to federally mandated benefits, these voluntary benefits play a vital role in staying competitive in the labor market. When selecting and prioritizing these voluntary employee benefits, organizations must balance their budgets while designing attractive benefits packages that will attract, retain, and motivate employees.

Health and Wellness Benefits

Health and wellness benefits constitute a significant cost to employers and are often extremely important to employees and their families, so consider your options carefully.

Medical Insurance

These are the most common medical insurance plans types to consider when building your employee benefits package:

- Preferred Provider Organization (PPO) – A group of physicians, dentists, hospitals, and other practitioners that contracts with employers, unions, or third-party administrators to provide employees with services at competitive rates. Employees have the ability to choose among physicians within the PPO arrangement. If the employee chooses to use a physician from outside the PPO network, then benefits are still paid, but the employee will typically have to pay a higher percentage of the cost.

- Health Maintenance Organization (HMO) – An organized system for the delivery of comprehensive health care services to a voluntarily enrolled population for a fixed, pre-negotiated payment.

- Point of Service Plan (POS) – A type of managed care medical plan where the level of benefits received depends on how an employee elects to receive care at the “point of service” that care begins. For example, if care begins with the primary care physician in the network, benefits would be higher than if care were received outside the network.

- Exclusive Provider Organization (EPO) – An alternative delivery system, composed of self-funded medical plans which resemble an HMO or a PPO. Participants are usually required to use only providers that are part of the system.

- Indemnity Plans – Medical plans that allow the participants the maximum amount of choice in selecting doctors, hospitals, and other providers of benefits. This is an insurance program that pays medical providers for services performed and defines the maximum amounts that will be paid for covered services.

Prescription drug plans are another important piece in the medical insurance puzzle. When selecting prescription drug plan options, organizations need to consider the co-payments and co-insurance fees that are the responsibility of employees for both generic and preferred drugs distributed by pharmacies or mail-order companies, evaluating costs to the employer versus costs to the employee.

Dental Insurance

Dental insurance plans typically cover diagnostic, preventive, restorative, periodontics, prosthodontics, and orthodontics dental care. Here are some common dental plan types to consider:

- Dental Preferred Provider Organization (DPPO) – A fee-for-service program that allows a participant to choose any dentist but provides financial incentives to choose dentists who are part of the preferred provider organization network.

- Dental Health Maintenance Organization (DHMO) – Provides a specified range of dental services for a set fee to participants. Participants must receive care from a participating provider. Dentists usually receive a set fee each month per participant, regardless of the care received by the participant.

- Dental Point of Service (DPOS) – A dental service plan that allows a member to use either a DPOS network dentist or to seek care from a dentist not in the DPOS network. Out-of-network care usually requires a higher out-of-pocket cost.

- Dental Exclusive Provider Organization (DEPO) – An alternative delivery system, composed of self-funded dental plans which resemble a DHMO or a DPPO. Participants are usually required to use only providers that are part of the system.

- Indemnity Plans – Dental plans that allow the participants the maximum amount of choice in selecting dentists and other providers of dental benefits. This is an insurance program that pays dental providers for services performed and defines the maximum amounts that will be paid for covered services.

- Dental Reimbursement Plan – These self-funded dental plans provide a simple, cost-effective way to provide limited dental benefits to employees and dependents. Participants are typically allowed to choose dental providers, pay for services directly, and receive reimbursement for expenses by the employer as outlined in the plan.

- Dental Discount Plan – An alternative to dental insurance that offers participants significant discounts on dental procedures. In this type of arrangement, participants pay a membership fee for access to a network of dental providers offering discounts to members.

Vision Insurance

Vision insurance typically covers some combination of the following costs associated with eye health: eye exams, eyeglass lenses, frames, contact lenses, prescription sunglasses, and corrective laser surgery. Vision coverage for employees can be offered using vision benefits plans, vision discount plans, or vision coverage within medical insurance plans.

Life Insurance

Life insurance is designed to provide monetary benefits to designated beneficiaries when the policy holder dies and can be an important part of a family’s long-term financial planning. As defined in ERI’s online glossary, life insurance is a “contract by which the insurer undertakes, in consideration of the payment of a premium (usually at stated periods), to pay a stipulated sum in the event of the death of the insured or of a third person in whose life the insured has an interest.”2 There are several life insurance types available, including these most common categories:

- Basic Life Insurance – A type of insurance that provides a lump-sum payment to beneficiaries upon the insured’s death. Typically, group-term life insurance coverage provided directly or indirectly by an employer does not exceed $50,000.

- Dependent Life Insurance – A group life insurance benefit providing death protection to the dependents of an employee covered under the plan.

- Excess Life Insurance – Employer-provided, group-term life insurance exceeding $50,000 is often referred to as “excess life insurance.” IRC section 79 provides exclusion for the first $50,000 of group term life insurance coverage provided under a policy carried directly or indirectly by an employer. There are no tax consequences if the total amount does not exceed $50,000. The imputed cost of coverage in excess of $50,000 must be included in income and is subject to Social Security and Medicare taxes.

- Supplemental Life Insurance – Additional insurance that supplements the coverage provided by a typical employer’s basic life insurance plan.

- Accidental Death & Dismemberment (AD&D) – A limited form of life insurance that pays benefits to the beneficiary if the cause of death is an accident.

Disability Insurance

Disability insurance benefits provide income to an insured individual, usually paid monthly, who is rendered unable to work and earn an income due to a disability. In the United States, the Social Security system provides government-based disability insurance benefits, but many organizations also offer this benefit via a private insurer. Disability insurance includes both short- and long-term disability insurance, as well as supplemental disability insurance, defined below:

- Short-Term Disability Insurance – Insurance that provides for income when an illness or injury prevents an employee from performing normal occupational duties for a period of less than one year or six months, depending on the plan.

- Long-Term Disability Insurance – Insurance that provides for income, usually a specified percentage of earnings that continues to retirement age or for a specified period of time, to employees who become disabled due to illness or accident and are unable to work for six months or longer.

- Supplemental Disability Insurance – Additional insurance that supplements the benefits provided by typical employer-provided, long-term disability insurance.

Employee Assistance Program

Employee Assistance Programs (EAP) are designed to help identify and resolve personal employee concerns that affect job performance. Some areas of concern may be substance abuse, marital problems, family troubles, stress, domestic violence, childcare, and eldercare. Services usually are provided by a third party to protect employee confidentiality.

Financial and Retirement Benefits

Aside from health and wellness benefits, financial and retirement benefits contribute a valuable portion of an employee’s total compensation package and can be a significant cost to employers. With a host of retirement plans available in the marketplace, organizations should consider their options with care. Here are some of the more common plans available:

- Pension Plan – According to the Department of Labor, “A pension plan is an employee benefit plan established or maintained by an employer or by an employee organization (such as a union), or both, that provides retirement income or defers income until termination of covered employment or beyond.”3

- 401(k) Plan – An employer-sponsored retirement savings plan that allows employees to contribute a portion of their pre-tax wages through payroll deductions.

- 403(b) Plan – An annuity that provides retirement income for employees of certain tax-exempt organizations derived from tax-deferred employee and/or employer contributions.

- 457 Plan – A non-qualified, tax-deferred compensation plan that works like a 401(k) and a 403(b) plan. Employees are allowed to defer compensation on a pre-tax basis through payroll deductions that further allow them to defer federal and sometimes state taxes until the assets are withdrawn.

- SEP-IRA Plan – A Simplified Employee Pension (SEP)-Individual Retirement Account (IRA) is a company-sponsored IRA that can be opened by even the smallest of businesses. Under an SEP-IRA, an employer can make deductible contributions to an employee’s existing IRA. SEP-IRAs are flexible for employers since the employer does not have to contribute every year.

- Roth 401(k) Savings Plan – A type of retirement savings plan that represents a unique combination of features of a Roth IRA and a traditional 401(k). The Roth 401(k) is funded with after-tax dollars for which taxes are paid in the current year. Typically, the earnings on Roth contributions are tax free as long as the distribution is made at least 5 years after the first Roth contribution and the employee has attained the age of 59½.

- Money Purchase Plan – A defined-contribution plan in which the amount of contribution that each employee receives from the employer is in proportion to the employee’s wages.

Time-off and Leave Benefits

Time-off and leave benefits may entail traditional leave plans or pooled-leave systems. Traditional leave plans typically consist of vacation, sick time, bereavement, personal leave, holidays, and floating holidays. A pooled-leave system combines all or part of paid leave into one pool, which is often favored by employers for ease of administration.

Additional Benefits

Larger organizations are increasingly offering additional benefits that enhance their total compensation packages. There are countless options available, but here are some additional benefits, including popular executive perquisites, that employers might consider:

- Phone or Internet Allowances

- Publications

- Association or Professional Dues

- Social or Athletic Club Dues

- Event Tickets or Conference Fees

- Relocation Expenses

- Corporate Housing

- Corporate Aircraft

- First Class, Spouse, or Conference Travel

- Car Allowance or Reserved Parking

- Personal or Home Security

- Financial or Legal Counseling

- Tax or Estate Planning

- Tax Gross-ups

- Flexible Executive Perks

- Charitable Contributions

- Dividends

- Plan-Based Contributions

- Severance Agreement

Step 2: Understand the Benchmarks for Competitors in Your Market

Start by gathering feedback from your workforce to assess their needs and preferences related to voluntary employee benefits. This will ensure that you target benefits that are relevant and valuable to your current employees. It is essential to then research benchmarks for employer-provided employee benefits customized for your geographic region, industry sector, and organization size. Knowing what your competitors are providing will help you build an attractive employee benefits package that stands out against your competitors and helps you hire and retain top talent. ERI provides two useful resources for benchmarking employee benefits: ERI’s Benefits Benchmarking Survey and the Benefits solution in ERI’s Salary Assessor.

Employee Benefits Benchmarking Survey

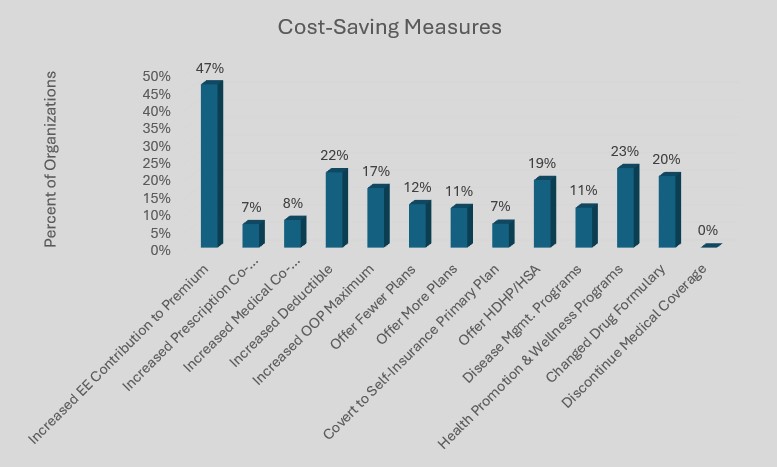

ERI’s Benefits Benchmarking Survey provides an invaluable resource to organizations in the process of building and updating competitive employee benefits packages. In addition to a comprehensive analysis of health care benefits, this annual survey includes detailed sections on life and disability insurance, paid time off, retirement, and executive prerequisites. Data cuts are provided by organization sector (privately and publicly owned for-profit, nonprofit, and government organizations), industry group, organization size (number of employees), and geographic region. Using this survey, you can drill down on actual costs and get specific details on employer-provided employee benefits that are relevant to your organization and its competitors, such as cost-saving measures.

Cost saving, or cost containment, is a strategy whereby an organization seeks to minimize the rising cost of certain health and welfare benefits by implementing selected programs that emphasize cost effectiveness. As seen in the chart below featured in ERI’s 2025 Benefits Benchmarking Survey, increased employee contributions to premiums was reported as the leading cost-saving measure used by 47% of survey respondents, followed by health promotion and wellness programs at 23% and increased deductibles at 22%.

For highlights of ERI’s 2025 Benefits Benchmarking Survey, download ERI’s recent whitepaper, “A Look into Employee Benefits: ERI’s 2025 Benefits Benchmarking Survey,” at www.erieri.com/whitepapers.

ERI’s 2025 Benefits Benchmarking Survey provided the definitions of benefits terms described in this blog post, unless noted otherwise.4

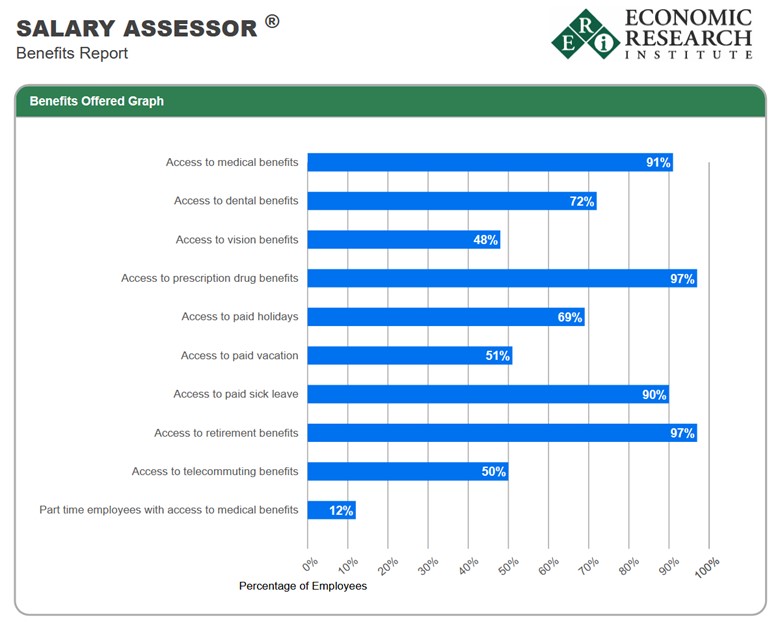

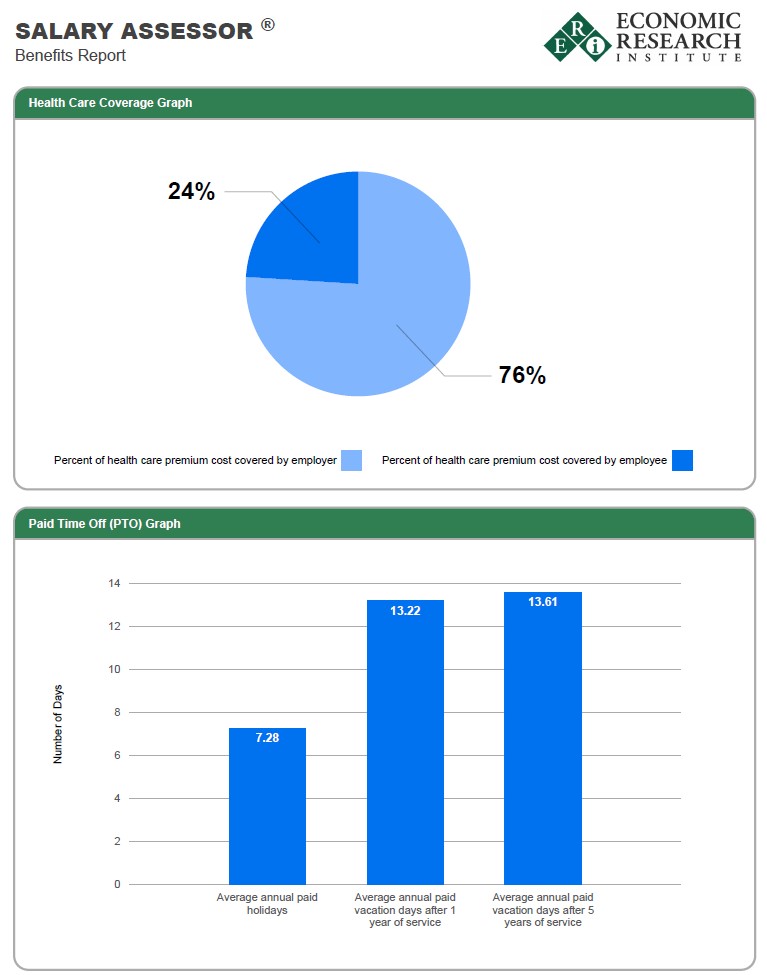

Salary Assessor – The Benefits Solution

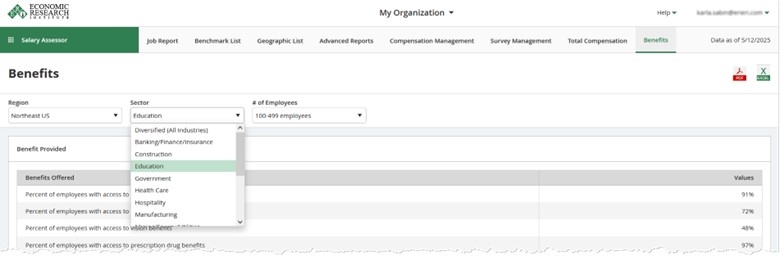

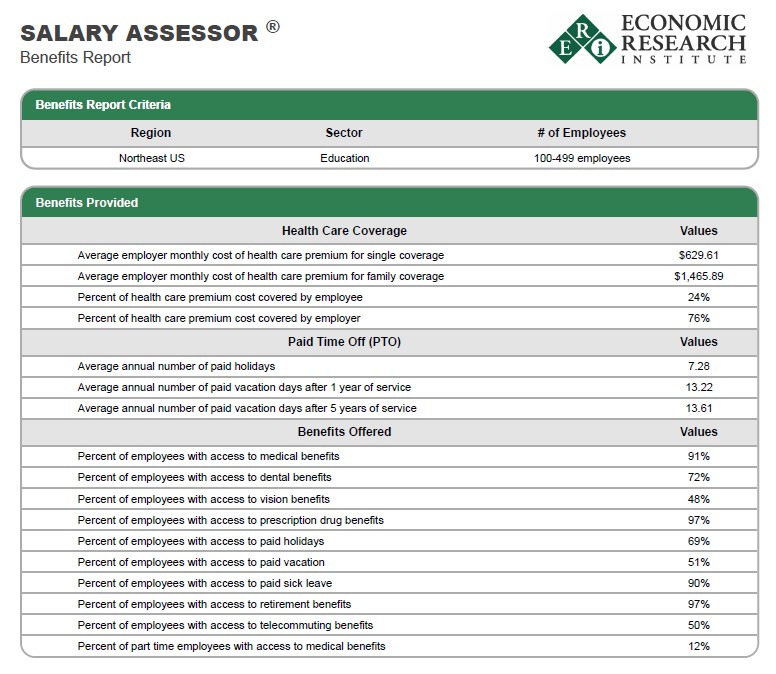

The Benefits solution in ERI’s Salary Assessor includes tables and charts analyzing data for benefits offered (including medical, dental, vision, prescription drug, paid holidays, paid vacation, paid sick leave, retirement, and telecommuting), health care coverage, and paid time off (PTO). Data may be specified by region, industry sector, and number of employees.

ERI’s Benefits solution helps you efficiently identify which benefits are being offered by comparable organizations in your market. See where you stand and how to improve your employee benefits packages without having to do laborious research. Easily export reports summarizing employee benefits trends to PDF or Excel to share with stakeholders involved in the process.

The Benefits solution in ERI’s Salary Assessor provides a robust dataset that includes information contributed by ERI’s Benefits Benchmarking Survey, as well as additional sources of employee benefits data.

Step 3: Identify Potential Vendors

Researching and ultimately selecting benefits providers can be a daunting task. When comparing numerous providers and various plan options, consider using an insurance broker to guide your process. In the process of balancing costs versus coverage, it will be important to compare premiums, deductibles, co-payments, and co-insurance rates across plans, as well as provider networks and employee preferences. Ensure that your choices are compliant with pertinent regulatory requirements at the state and federal level, such as the provisions outlined in the Affordable Care Act (ACA).

Step 4: Budget and Administer Your Employee Benefits Plan

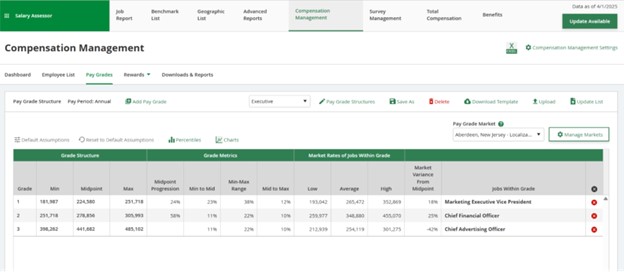

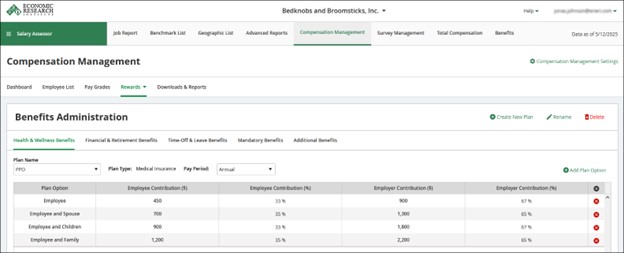

Once you have selected your benefits offerings, the next step entails budgeting and administering your benefits plans. The Compensation Management solution in ERI’s Salary Assessor provides the data and tools that you will need to effectively and efficiently manage benefits in your organization. Using the Benefits Administration feature in Compensation Management, you can easily define benefits plan options, including health and wellness benefits, financial and retirement benefits, time-off and leave benefits, mandatory benefits, and additional benefits, to administer in your organization. The benefits administration platform will help you define employee and employer contributions, as well as other pertinent information such as accrual rates for time-off benefits, employer matching for retirement benefits, and more, so that you can manage your employee benefits plans accurately while keeping an eye on your overall budget. You can create a number of hypothetical scenarios to strategize your employee benefits plan and ensure that you not only satisfy budget requirements but also create a competitive benefits package that will be attractive to new and existing employees.

Step 5: Communicate Your Benefits Plan

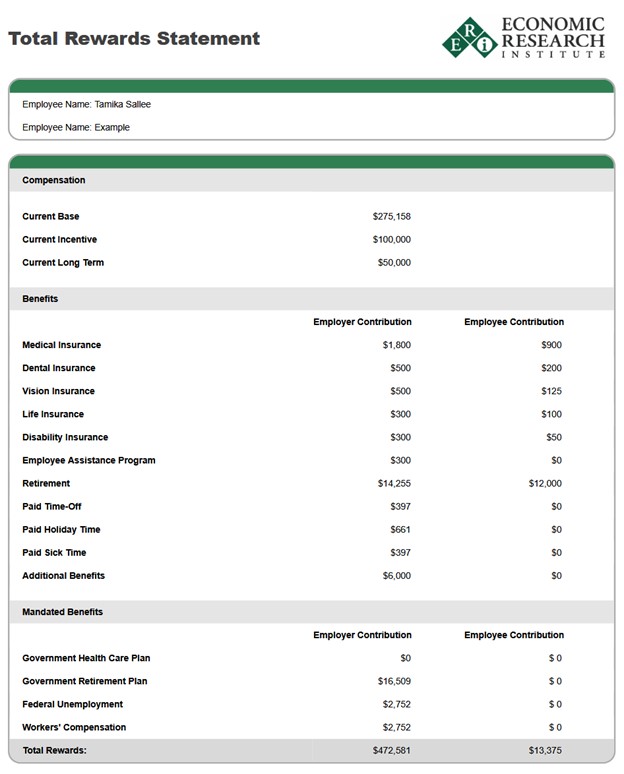

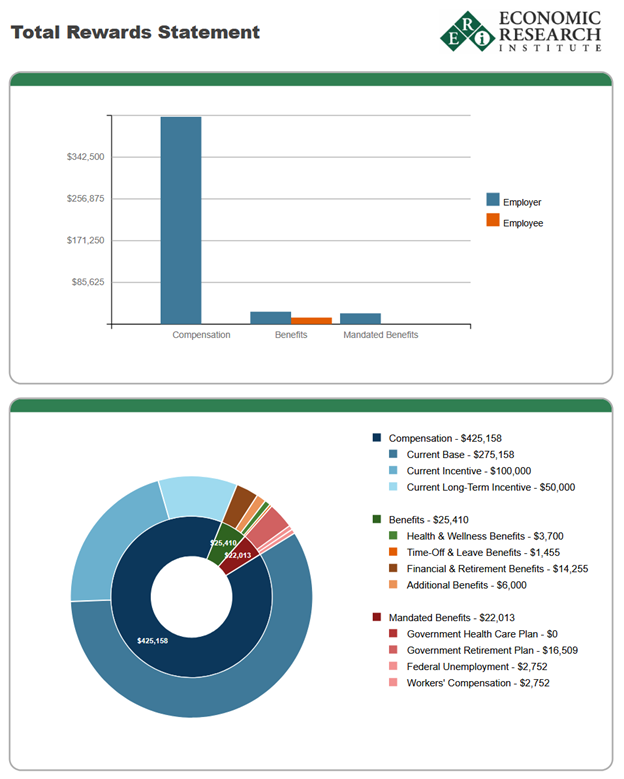

Once you have designed your overall benefits plan in Benefits Administration and selected specific benefits options for individual employees in the Employee List of Compensation Management, you can export a Total Rewards Statement, in addition to an array of other valuable reports, to share with stakeholders in your organization. The Total Rewards Statement provides a complete breakdown of individual employee pay, including current base, incentive, and long-term incentive compensation, plus optional and mandated benefits, with employee and employer contributions for each benefit option. Use this report to communicate your employee benefits plan to individual employees, creating both transparency and trust, as well as others on your team.

Step 6: Review and Adjust Your Benefits Package

To remain competitive, you should conduct annual evaluations of your benefits plan and implement updates, as needed. This will ensure that you stay abreast of current benefits trends among your competitors, respond to changes in costs such as increased insurance premiums, align your plan with ongoing budgetary needs, and keep your finger on the pulse of employee preferences. Using ERI’s Compensation Management platform, you will have constant access to current and accurate compensation and benefits survey data so that you can benchmark employee benefits based on real-time data. The platform makes it easy to update the details of your benefits plan, analyze the impact of modifications, and communicate changes to employees.

Conclusion

Building a competitive employee benefits package that attracts, retains, and motivates employees, while aligning with an organization’s budgetary requirements, is critical for organizations of all sizes. HR and compensation professionals need to stay on top of current trends in employee benefits with data customized to reflect comparable organizations in their market. ERI’s Benefits Benchmarking Survey provides an in-depth report of employer-provided employee non-cash benefits from a broad range of participating organizations, with actual costs and coverage details reported by organization sector (privately and publicly owned for-profit, nonprofit, and government organizations), industry group, organization size (number of employees), and geographic region. For a broader analysis, the Benefits solution in ERI’s Salary Assessor provides a robust database of employee benefits data, including information contributed by the Benefits Benchmarking Survey and additional sources of data, in an easy-to-use online platform that helps you quickly drill down on the data you need and export customized reports.

Beyond benchmarking employee benefits data from comparable organizations, HR and compensation professionals need to carefully design, administer, communicate, and maintain their benefits plans. Using the Benefits Administration feature in the Compensation Management solution of ERI’s Salary Assessor, organizations can efficiently and effectively manage all aspects of their employee benefits packages, including budget adherence and ongoing annual reviews. ERI’s Total Rewards Statement provides a complete breakdown of individual employee pay with employee and employer contributions to optional and mandated benefits, helping organizations communicate their benefits decisions to both stakeholders and employees. ERI is here to help you with all the steps involved in building a competitive employee benefits package, saving you time while ensuring accuracy.

For more information about ERI’s Assessor Platform, please sign up for a guided tour and let us show you how we can help you create and maintain a competitive benefits package tailored to your organization.

References

- “Economic safety net: Social Security and other legally required benefits.” Employer Costs for Employee Compensation (ECEC), U.S. Bureau of Labor Statistics, bls.gov/ecec/factsheets/ecec-legally-required-benefits-factsheet.htm.

- ERI Economic Research Institute. “Compensation Glossary.” ERI Resources, erieri.com/glossary.

- “Retirement Plans Benefits and Savings.” S. Department of Labor, www.dol.gov/general/topic/retirement.

- ERI Economic Research Institute. “2025 Benefits Benchmarking Survey.” ERI Salary Surveys, Apr. 2025, www.erieri.com/salarysurveys/benefits