Originally posted on 2/25/16 and updated on 7/26/16

In the U.S., the Department of Labor has recently amended the Fair Labor Standards Act (FLSA), increasing labor costs, particularly for service industry sectors. The changes may require any employees earning less than $913 per week ($47,476 annually) to be paid overtime once the standard workweek hours are exceeded. At ERI, we are helping organizations navigate FLSA minimum wage laws and job analysis requirements by providing technology and compensation analytics to holistically evaluate the business impact on job classifications and labor costs.

Consider some issues expressed by HR leaders on these matters:

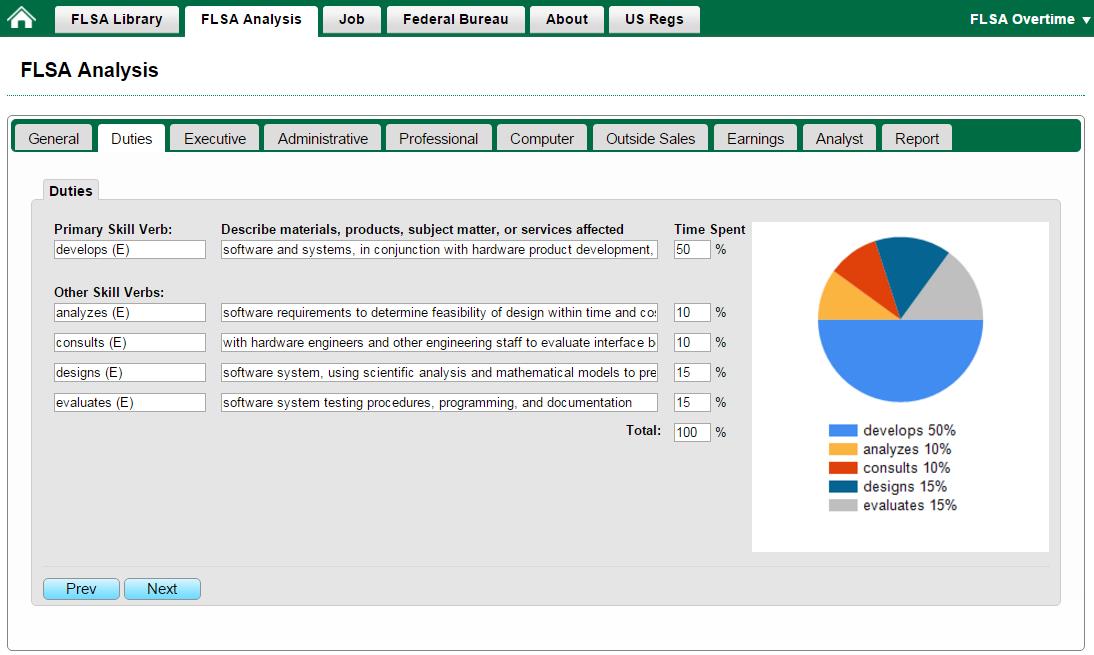

The complexity of FLSA is associated with overtime pay that requires job analysis of actual responsibilities performed, minimum wage, salary thresholds, record keeping (tied to a standard workweek), and regulatory variations at the federal/state/city-level. From an organizational development and job classification perspective, having job analysis software specifically mapped to FLSA regulations can be invaluable. ERI’s Occupational Assessor (OA) is helping HR business partners and OD experts document and reasonably predict FLSA classifications based on their knowledge of the job relative to each criterion for the exemption tests. The benefit of the OA is selecting a job match from over 6,000 job descriptions already analyzed by ERI industrial psychology PhD staff, as well as conducting analysis for jobs that cannot be matched with benchmark job descriptions. Below is a series of screen shots from ERI’s Occupational Assessor FLSA Analysis tool:

Duties Tab – The Duties tab summarizes primary and secondary job responsibilities based on the job analyst’s knowledge of the job duties. Some states may have bright line tests with specific percent of duties thresholds (e.g., California at 50% exemption duties requirement). The Duties tab is designed to evaluate the percent of duties relative to the whole job.

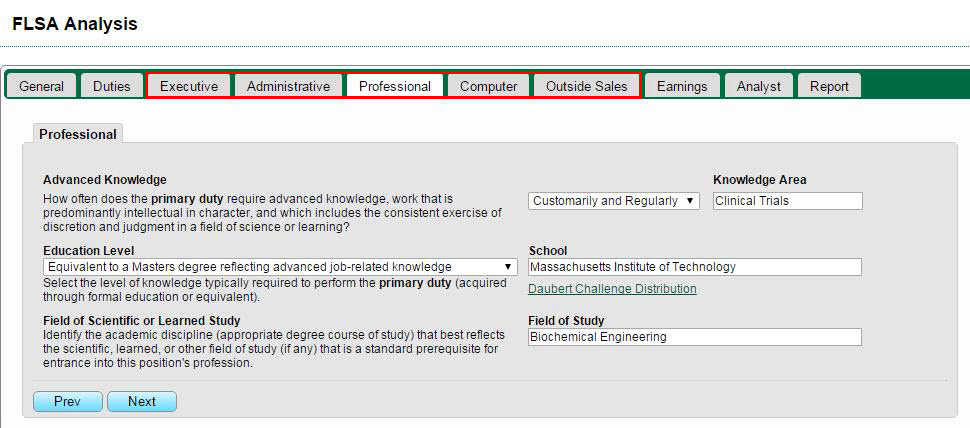

Professional Tab – The Professional exemption test is one of the five exemptions that precludes an employer from having to pay overtime wages. The Professional test requires the job to be assessed in terms of advanced knowledge, education level, and scientific and learned study requirements. All three specific criteria must be present (actually performed) in the job. Similar assessments for Executive, Administrative, Computer, and Outside Sales can be evaluated in the respective OA tabs. Some jobs may pass more than one exemption.

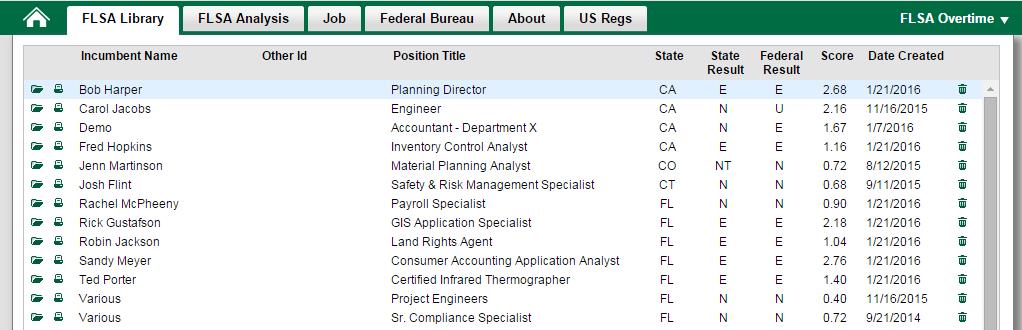

FLSA Library Tab – This tab provides centralized, secure access of job analyses and resultant FLSA classifications. When business operations change that significantly affect job duties, you can easily review related job content and easily update the job duties in OA and evaluate the impact (if any) on the FLSA classification.

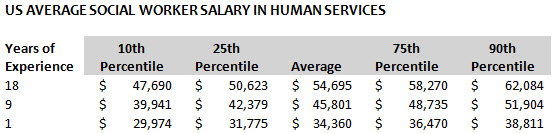

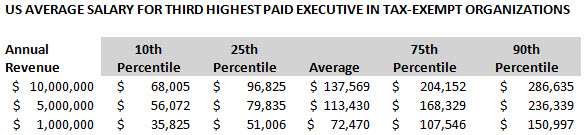

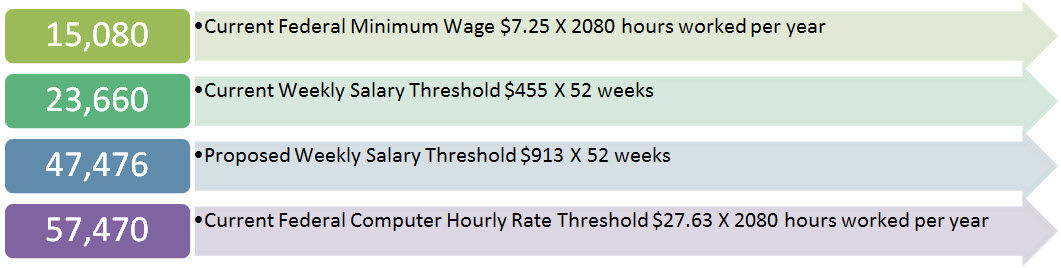

In light of the new legislation, another important part of this assessment is from a labor cost perspective. It is important to evaluate the business impact of the salary threshold increase to $913/week, particularly on exempt employees currently making less than that. Consider some of these key annualized labor costs to incorporate into your analysis:

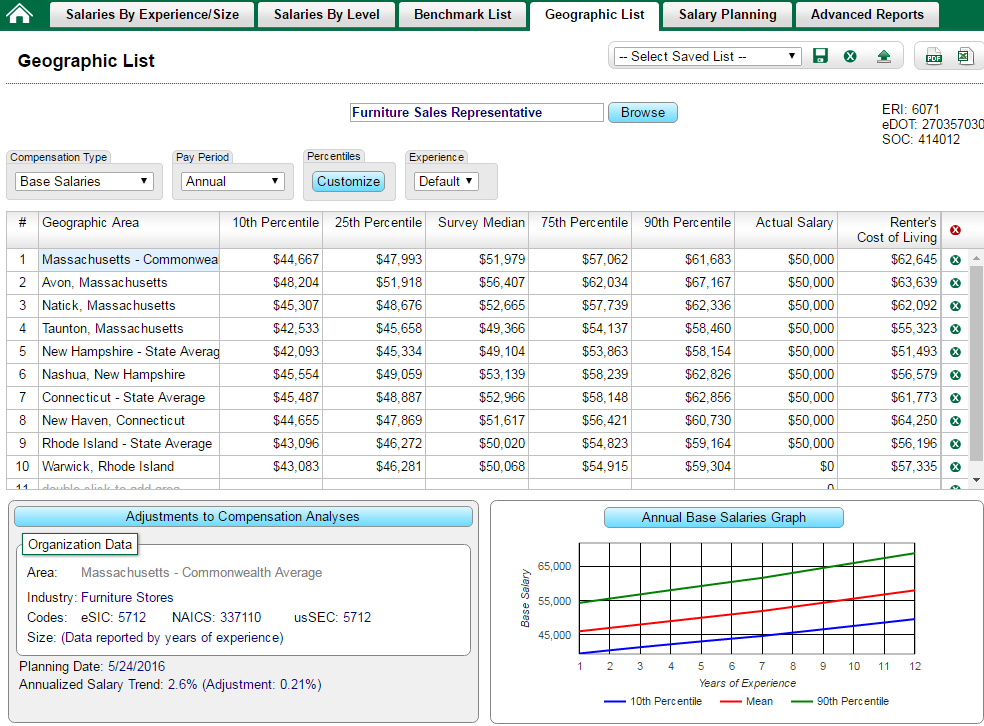

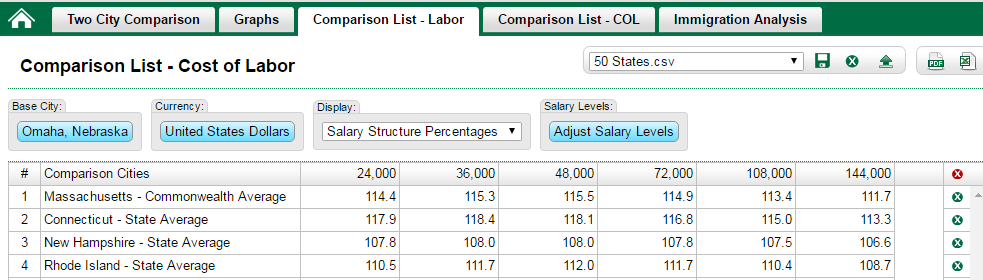

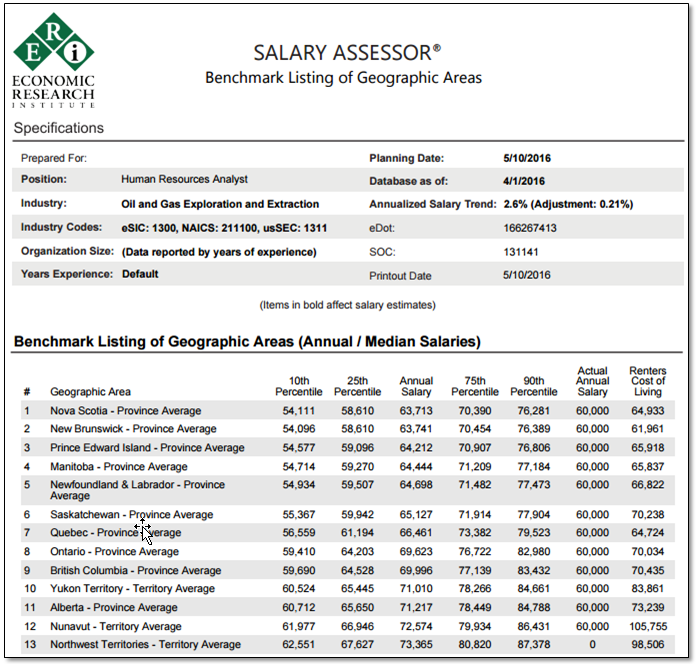

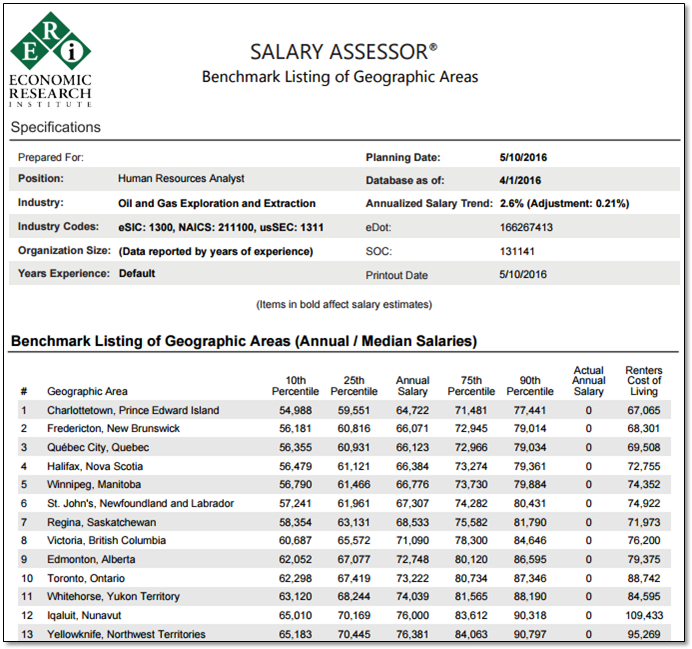

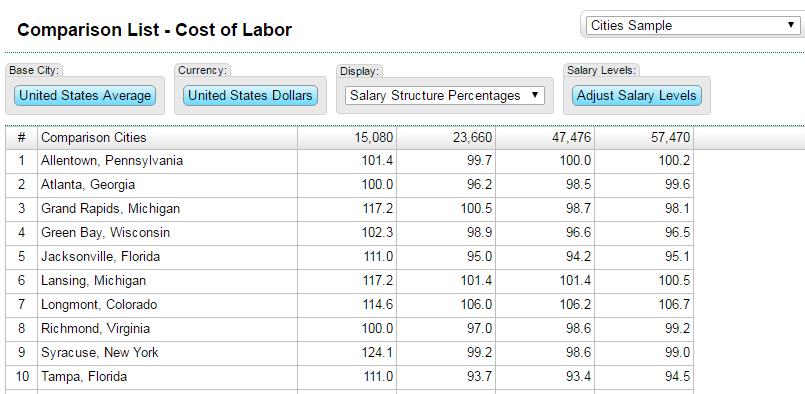

Another compensation analytics tool is ERI’s Geographic Assessor (GA), which provides geographic labor differentials that can be customized to the user defined labor costs. For purposes of the new FLSA salary threshold change, let’s analyze the geographic differentials relative to the four annualized labor costs mentioned above by adjusting the salary levels. Typically, the salary level represents the salary midpoints of organization’s compensation structure. Below is a Comparison List of cost of labor differentials for 10 cities.

Geographic Assessor – The Comparison List includes adjusted salary levels as follows:

Some insight HR leaders gain from this GA Comparison List table follow:

- For operations in Atlanta, GA, you will lose the competitive advantage of geographic labor differentials if the federal requirement increases to $47,476. Atlanta is currently 96.2% of the US Average.

- Syracuse, NY, has the highest state-level minimum wage, which is currently 24.1% about the federal rate (e.g., $9.00/hour versus $7.25/hour).

- Allentown, PA, has the least variation in labor differential in the location across all job levels. The differentials range from 99.7% to 101.4% of the US Average.

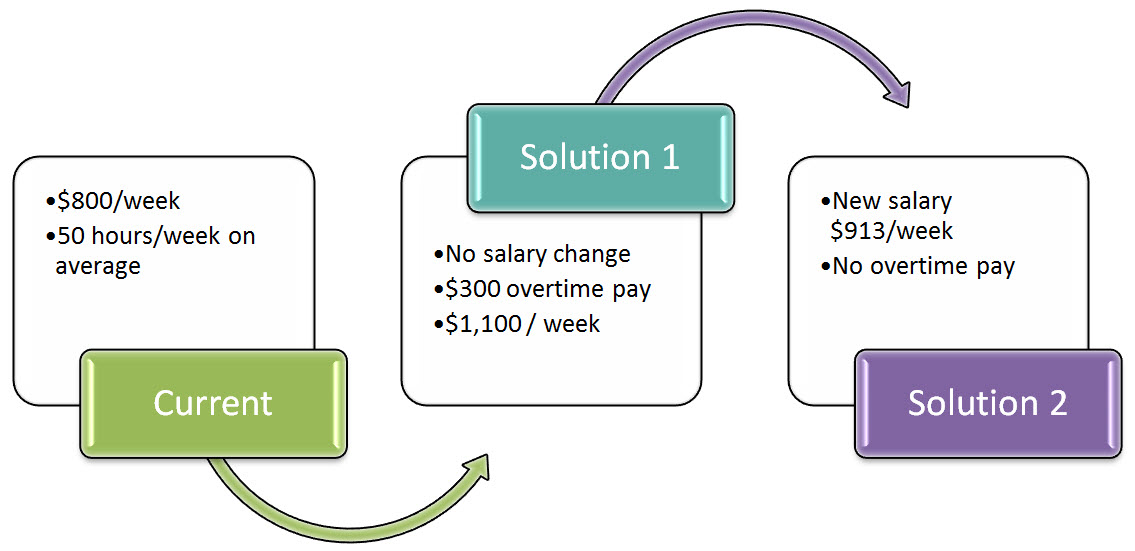

Internally the labor costs analysis will focus on those exempt jobs currently paid less than $913 and review of historical records for their actual hours worked, calculating overtime pay with current salary compared to no overtime with a new threshold:

Although Solution 1 may seem like a win for the employee, from an employee relations perspective, having to revert back to tracking and reporting hours work versus taking ownership of results and self-managing hours will likely have more of a negative effect on employee satisfaction. Whereas, in Solution 2, increasing the salary to new threshold will result in high pay level yet still have the employee performing the same job with the same level of commitment and motivation as a manager.

Summary

Organizations, especially service industries, have business models that are sensitive to internal and external factors that affect labor costs. The new FLSA salary threshold of $913/week is more than double the current $455/week requirement. Evaluate the implications of adjusting the salary levels and changing the FLSA classifications for the jobs from a financial impact, as well as organization development perspective. For more information about FLSA job analysis and related technology solutions, call our “best in class” service team at or visit www.erieri.com.

ERI Economic Research Institute compiles the most robust salary, cost-of-living, and executive compensation survey data available, with current market data for more than 1,000 industry sectors.

ERI’s Assessor Series® – Solutions for every compensation decision