Assisting employees in preparing for the milestone that is retirement is a rewarding but often complex process. Although retirement may seem to be a lifetime away for younger employees, planning for the future requires careful selection of advantageous plans that optimize retirement savings. A tried-and-true method of planning and updating retirement plans involves benchmarking internal practices against the market. By doing so, HR and compensation professionals can design data-driven retirement packages that are both competitive and enticing to current and prospective employees.

To assist with this process, ERI Economic Research Institute proudly presents its 2025 Benefits Benchmarking Survey. The focus of this annual survey report is to offer insight into valuable data to benchmark an organization’s benefits practices with those of other employers in the external marketplace. Having the ability to accurately benchmark employer-sponsored employee benefits will help HR and compensation analysts evaluate and improve the effectiveness of their overall compensation and benefits strategy and provide an edge over competing organizations.

The eighteenth edition of this survey includes a comprehensive analysis of employee benefits, offering detailed data cuts for general benefits, medical benefits, life and disability insurance, employee leave practices, retirement, and executive prerequisites. This survey also contributes benefits information to the robust database provided in ERI’s Assessor Platform, allowing compensation analysts to more accurately benchmark and plan benefits packages.

Although health care will continue to be the primary concern for employers and employees alike, other benefits are just as important to consider when planning a well-rounded benefits package. A comprehensive and attractive benefits package is essential to attracting, retaining, and motivating top talent.

In this specific article, we look at the trends and data in employer-sponsored retirement plans, as reported by ERI in the 2025 Benefits Benchmarking Survey.

ERI Economic Research Institute’s Survey Methodology

ERI’s survey questionnaires were designed and distributed for the 2025 Benefits Benchmarking Survey in October 2024. Participation was solicited from employers in the public, private, and nonprofit sectors, as well as government entities in the United States. Data input was collected in the period from October 1, 2024, to February 3, 2025. The requested effective date of benefits data was January 1, 2025.

Eighty-eight (88) U.S. organizations contributed data to the survey. Characteristics of participants varied greatly and are illustrated in the “Characteristics of Participating Organizations” section of the survey. Seventeen (17) industry groups are represented, including nonprofit organizations and government entities.

Investing in Rewarding Retirement Packages for Employees

Employer-sponsored retirement plans are more than just a benefit for employees. They are a strategic investment by a company to recruit and retain top talent. Offering attractive retirement benefits for employees not only invests in their future but also contributes to employee engagement and productivity.

A well-structured retirement plan begins with identifying organizational goals and employee expectations. Each company works within a unique context and might prioritize different needs and concerns. For example, established companies might plan their rewards with employee retention in mind, while start-ups or growing companies may focus more on flexibility. Whichever may be the concern, understanding an organization’s specific goals is crucial when planning and benchmarking retirement plans.

Additionally, it is important to identify particular aspects of retirement packages that allow benefits coordinators to strategically plan benefits in a highly competitive market. These are just a few things to keep in mind to when benchmarking internal practices against the market:

- Understand employee demographics and expectations.

- Be knowledgeable of the various retirement plans available.

- Review budget and legal standards to determine employer-contribution limits.

- Consider retirement plan options that best align with organizational goals.

Benchmarking Data to Plan Competitive Retirement Packages

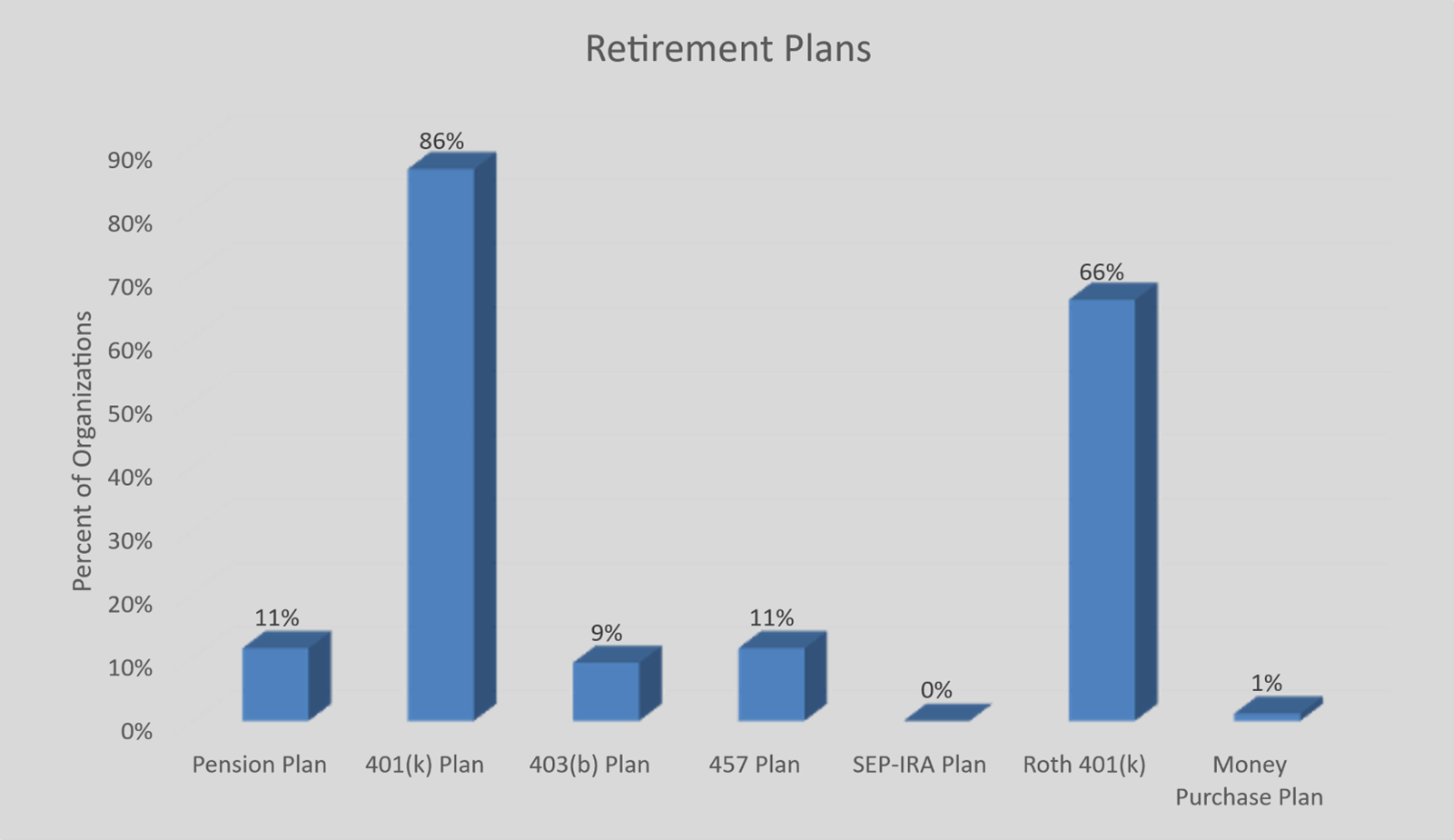

As mentioned, to successfully design competitive retirement packages, it is important to know the various retirement plans that can be offered by employers in the United States. According to ERI’s 2025 Benefits Benchmarking Survey, eighty-five (85) of the eighty-eight (88) respondents offered some type of retirement plan to employees. Eighty-six percent (86%) of the organizations providing a retirement plan offered a 401(k) plan1. The following chart demonstrates the most common types of retirement plans offered by employers according to survey participants, with definitions provided below:

- 401(k) Plan – An employer-sponsored retirement savings plan that allows employees to contribute a portion of their pre-tax wages through payroll deductions.

- Roth 401(k) Plan – A type of retirement savings plan that represents a unique combination of features of a Roth IRA and a traditional 401(k). The Roth 401(k) is funded with after-tax dollars for which taxes are paid in the current year. Typically, the earnings on Roth contributions are tax free as long as the distribution is made at least 5 years after the first Roth contribution and the employee has attained the age of 59½.

- Pension Equity Plan – A defined-benefit plan that provides an annuity or lump-sum benefit upon end of employment. Pension equity plans define benefits in terms of a current lump-sum value. Annual credits can be based on age, service, or a combination of both. The plan determines the total benefits by providing a “schedule of percentages” that are accumulated throughout the work life of the employee.

- 457 Plan – A non-qualified tax-deferred compensation plan, typically for local or state government or tax-exempt organizations, that works like a 401(k) and a 403(b) plan. Employees are allowed to defer compensation on a pre-tax basis through payroll deductions that further allow them to defer federal and sometimes state taxes until the assets are withdrawn.

- 403(b) Plan – An annuity that provides retirement income for employees of certain tax-exempt organizations derived from tax-deferred employee and/or employer contributions.

- Money Purchase Plan – A defined-contribution plan in which the amount of contribution that each employee receives from the employer is in proportion to the employee’s wages.

- SEP-IRA Plan – A Simplified Employee Pension (SEP)-Individual Retirement Account (IRA) is a company-sponsored IRA that can be opened by even the smallest of businesses. Under an SEP-IRA, an employer can make deductible contributions to an employee’s existing IRA. SEP-IRAs are flexible for employers since the employer does not have to contribute every year.

Using reliable survey data, HR and compensation professionals will get current market insights into these popular retirement plan types. To help analysts drill down on the data that most accurately reflect comparable organizations competing for talent, ERI provides data cuts by organization sector (privately and publicly owned for-profit, nonprofit, and government organizations), industry group, geographic region, and organization size (number of employees).

Beyond understanding the various types of employer-sponsored retirement plans available, there are fundamental components in the design of retirement benefits to consider. To assist in evaluating current market trends, ERI’s 2025 Benefits Benchmarking Survey reports survey participant responses for these retirement plan options:

Employer Contributions to Defined-Contribution Plans

- Matching Contributions

- Fixed Contributions

- Discretionary Contributions

- Both Matching and Non-Matching Contributions

Vesting Schedules

- 100% Immediate

- Cliff Vesting

- Graded Vesting

Special Plan Provisions in Defined-Contribution Plans

- Participant-Directed Investment

- Participant Loans

- Auto Enrollment

- Hardship Withdrawals

- In-Service Withdrawals

Types of Defined Benefit Plans

- Final Average

- Career Average

- Cash Balance

- Pension Equity

Use ERI’s Benefits Benchmarking Survey Data to Transform Benefits Planning

According to the American Psychological Association, 63% of adults aged 45-64 in 2023 reported that money and the economy were a significant stressor, a huge jump from the 45% reported in the same demographic in 20192. In short, finance is a large concern for many Americans. This is why employer-sponsored retirement plans are essential in retaining employees, while also providing workers with financial stability.

Creating data-driven rewards packages is a major part of this process and begins with planning and benchmarking benefits practices. Benchmarking external market data is imperative to benefits planning, in particular, because it enables analysts to contextualize their practices against organizations competing for the same labor. For example, ERI’s 2025 Benefits Benchmarking Survey reported these average maximums for employer-matching contributions from all U.S. survey respondents:

| $0.25 for each $1 up to | $0.50 for each $1 up to | $0.75 for each $1 up to | $1.00 for each $1 up to | Average Contribution as % of Base |

|---|---|---|---|---|

| 4.0% | 6.7% | -- | 7.1% | 4.6% |

In interpreting the data to inform benefits planning, analysts will be able to identify the more market-popular matching contribution maximums, with 7.1% of respondents contributing $1 for each $1. The data provided will help planners evaluate competitive trends in the market and revise internal practices accordingly, ensuring that their retirement benefits packages are not only attractive to employees but also fit the organization’s budget and long-term goals.

This is why ERI strives to provide HR and compensation professionals with the latest and most accurate data vetted by PhD-level scientists. Using current market data, like that reported in our 2025 Benefits Benchmarking Survey, analysts can reliably benchmark retirement plans and other employee benefits. Data from ERI’s 2025 Benefits Benchmarking Survey also contributes to the extensive database in ERI’s Salary Assessor, providing for more precise and informed benchmarking and analytics. ERI’s Assessor Platform gives HR and compensation experts immediate online access to a robust database, consisting of compensation and benefits surveys, for both benchmarking and more comprehensive compensation management. Optimize your benefits planning with ERI’s Assessor Platform. Try a free demo today!

Sources:

- ERI Economic Research Institute. “2025 Benefits Benchmarking Survey.” ERI Salary Surveys, Apr. 2025, www.erieri.com/salarysurveys/benefits.

- “Stress in America 2023: A Nation Recovering from Collective Trauma.” American Psychological Association, Nov. 2023, www.apa.org/news/press/releases/stress/2023/collective-trauma-recovery.