Looking to Benchmark Pay?

Option Pricing Technique

Placing a value on options or grants based upon future stock performance and economic variables requires an option pricing technique. These techniques are complex mathematical models, but there are many calculators on the Internet that will perform the calculation, if you provide the information requested. ERI has a Black-Scholes calculator on its website.

These techniques have become important because organizations must calculate the stock option value each period they are awarded to participants. The Securities and Exchange Commission requires that stock options amounts be recorded in the yearly filing of the corporation's 10-K and proxy statements. Since the advent of accounting regulations FAS 123R in 2005 and its subsequent replacement, ASC 718, in 2009, companies have reported the fair market value (FMV) of all equity-based compensation which becomes an expense that directly affects the income statement.

The Binomial (Lattice) and Black-Scholes methods are the most common option pricing techniques. Understanding the fundamental design of these models can help the total rewards practitioner to manage the information requirements for disclosure, to assess effective equity plan designs, and to enhance employee communications. The Black-Scholes and Binomial models have improved valuation results since they take into consideration plan design characteristics, allow for sensitivity analysis with volatility assumptions, and reflect exercise behavior realities. The standard inputs to both models include:

- Current stock price

- Exercise price

- Risk free interest rate

- Expected dividends on stock

- Expected stock price volatility

- Expected term of option

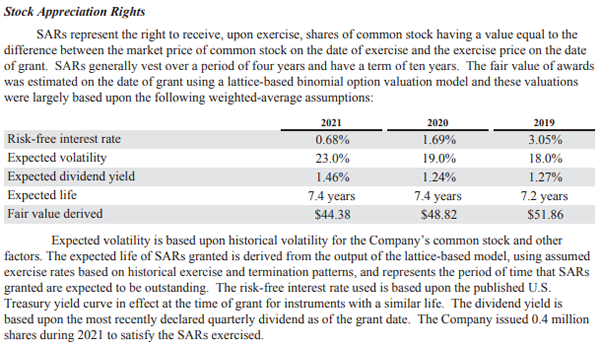

Determining the value for the expected option term relies on the behavior of the employees who hold options and is less predictable. For private firms (who tend to use Black-Scholes), the expected volatility of their stock is also less predictable since they have no trading history like public firms. The stock price, exercise price, risk free interest rate, and expected dividends tend to be more stable inputs to the models. Becton Dickinson adopted the binomial model in 2004 and a recent Form 10-K Report disclosed sets of 3-years of assumptions and inputs used in the valuing of its stock appreciation rights (SARs):

Model Assumptions:

Source: Becton Dickinson

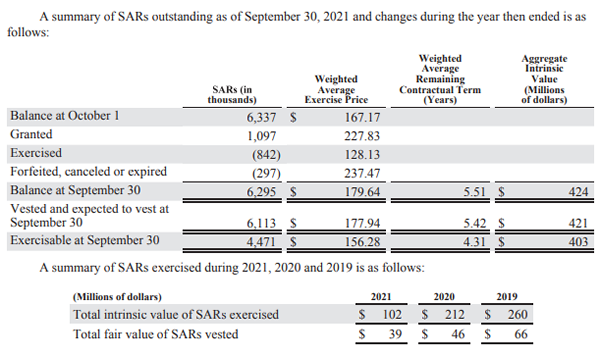

Source: Becton Dickinson

For both the Binomial and Black-Scholes models, there is a generic version plus several variations that capture more granular assumptions that make the models more predictive, albeit more complex. Depending on the complexity of the equity programs, the business model in which the organization operates, and the cost/benefit trade-off of adopting a more complex pricing model, it can incorporate one or more of these additional variables:

- Expected holding period and exercise history (both pre- and post-termination).

- Vesting period and company-specific exercise rules.

- Termination rate or forfeiture rate (the probability of a vested option being canceled).

- Blackout periods and arrangements for automatic exercise.

For those interested in learning how to use this formula to model the future value of stock options, we refer you to DLC Course 22: Black-Scholes Valuations.

Source: ERI Black-Scholes Calculator

Memory Jogger

Option pricing techniques are used to: