Looking to Benchmark Pay?

Large Group Incentive Plans

A large group incentive plan rewards the accomplishment of specific financial and/or non-financial results over what is typically an annual performance period. The vast majority of organizations currently manage their variable compensation program to a large group annual incentive plan.

Design of a Large Group Incentive Plan

Eligibility

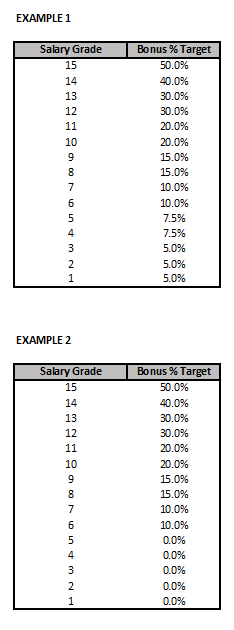

Eligibility is typically organization-wide, division-wide, or may include a significant group of employees with a minimum threshold for eligibility (e.g., salary grade). Many organizations will provide eligibility as a percent of base pay or base salary midpoint according to salary grade or level. This will also ensure the bonus percent at target is market competitive as it will increase consistently with grade and the labor market. Below are two examples of bonus eligibility by Salary Grade administered as a percent of actual base salary at target:

You will see that Example 1 displays salary grade by an increasing bonus percent target that changes in frequent increments, wheras Example 2 includes only senior professional/management employees and above for bonus eligibility. Market practice and desired plan design should be the determining factors for bonus percent eligibility. The minimum percentage for bonus target should not be less than 5% to ensure the bonus payouts provide a sufficient payout for participation. Also, keep in mind that if too much pay at risk is provided to lower-level employees, their required income for day-to-day living expenses is also at risk. In the event of non-payout, this may cause employee relations issues and potential turnover at this level.

Plan Metrics

When designing a Large Group Incentive Plan, up to five financial and/or non-financial metrics over a designated performance period are typically identified as plan objectives. Most organizations will select two or three financial metrics with revenue, EBITDA, earnings per share, and operating income being the most frequently used. Cash flow, net income, and revenue growth are also commonly used metrics.

Non-financial metrics may typically include Management by Objectives (MBO) attainment, performance, customer satisfaction, and operational efficiency.

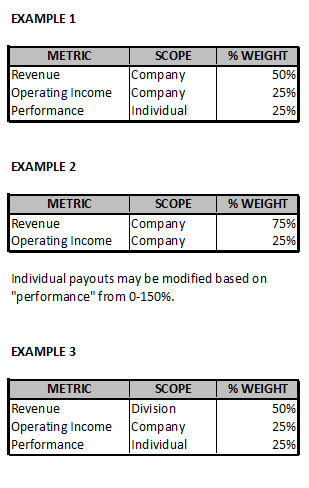

The examples below show two or three metrics, the percent weight applied, and the scope of the business results being assessed:

In all three cases, individual performance is also measured as a metric for payout. In Example 2, a bonus pool is generated based on the financial metrics (revenue and operating income), and payouts are based upon MBO attainment/performance rating from 0-150%. Keep in mind when using a performance modifier that the average participant rating should be 100% to ensure actual payouts are managed within the pool.

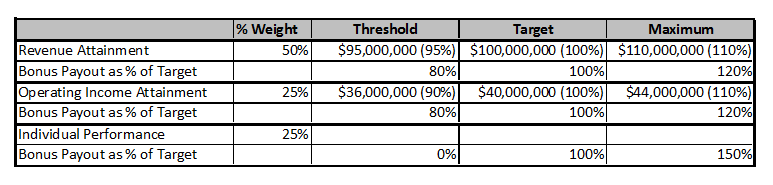

In addition to determining the financial metrics for payout, a threshold, target, and maximum is added to support the minimum and maximum financial attainments needed for the incentive plan. So, for example, the design could be as follows:

So, $95,000,000 would be the required revenue prior to any payout being made. The plan would pay 100% target upon revenue attainment of $100,000,000. The maximum payout could be paid at $110,000,000 revenue attainment. Some plans are managed without a maximum payout. However, unexpected events and results can influence a maximum payout, so a maximum payout formula ensures the company is protected in these cases.

The next step in the process is to establish the payout provisions of the plan as follows:

Bonus Payout Matrix

In the above example, you can see the bonus payouts have been added to revenue attainment requirements and include a minimum, target, and maximum payouts. Frequently, bonus payouts are prorated for attainments between percentages and should be added to the plan document. Note that the percentage for bonus payout is different from the percentage for revenue attainment.

The other metrics can be added to the matrix as well. Be sure to use separate attainment percentages based on the specific metric being assessed.

Memory Jogger

You are considering implementing a large group incentive plan for your company. What financial and non-financial metrics would be appropriate to recognize for the performance period?