Each quarter, ERI examines the rates at which compensation has increased and provides guidance on expected increases for the upcoming year. These rates are calculated using ERI’s Salary Assessor and ERI’s Salary Increase Survey & Forecast. In the context of this paper, results represent actual growth reported in ERI’s Salary Assessor over periods ranging from one quarter to twenty years.

Actual compensation movement in the second quarter of 2023 (published July 1, 2023) saw a higher level of growth at 1.17%, above April’s 1.1% rate, but below January’s 1.39% growth. The past 4 quarters have seen higher-than-average growth, with 4.95% growth since the October 2022 data release. This rate of growth is the second highest since ERI started tracking year-over-year (YOY) growth rates, with the previous peak at the end of 2007 (5.32%). It may be surprising that the YOY growth rate hit a new high this quarter, with the current quarter showing a lower rate than the January 1 growth rate (1.39%). However, this is due to the July 1, 2022, rate of 0.71% dropping off of the average calculation.

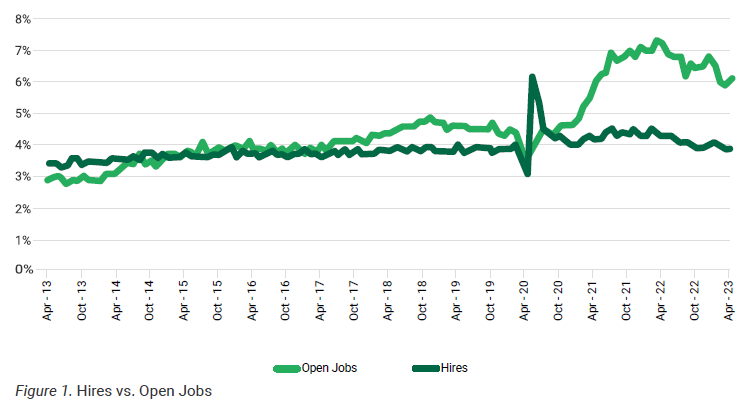

Current labor market data indicate a softer market than spring/summer 2022, but one that remains competitive. An examination of the current number of job openings indicates a high number of open jobs in the United States, with an open job rate of 6.1%, which is higher than the 10-year average open job rate of 4.57% However, it is down from the high of 7.3% in March 2022. Figure 1 below shows the historical difference between the rate of open jobs in the economy versus the rate at which employees are hired. A gap between the number of open jobs and the number of employees who are hired indicates that organizations are not able to hire all the employees that they would like. This can lead to organizations needing to raise compensation rates to hire the employees needed.

The rate at which employees are quitting is currently 2.4%, which is down from its high of 2.9% in April; but it is still higher than the 10-year average of 2.23%. These trends point to a softening labor market that is still tight, which indicates higher compensation growth. Further

softening may reduce this pressure, but that level does not appear to have been reached yet. These trends are supported by overall labor market demographics. Specifically, the unemployment rate was 3.7%, which is up from July 2022’s low of 3.5%, but still generally considered full employment. The prime-age population ratio (EPOP) has reached a new local peak at 80.7%, which is 0.2% above last quarter’s rate. Additionally, the 30-year average EPOP is 78.6%, which is below the current participation rate and above the rate immediately prior to the start of the recent pandemic (80.5%). The current EPOP is below the all-time high, which was 81.9% in April 2000.

Of course, the labor market is not the full story. At the time of writing, the inflation rate stands at 4%, which is down 5.1% since the high in June of 2022. These trends appear to indicate a reduction from peak inflation, which may have a tempering effect on compensation increases. Inflation can influence the growth of compensation, and the extent of that influence also varies depending on the level of inflation, with high

inflation being related to higher levels of compensation growth. Inflation is above the target rate of 2%, so we may continue to see higher levels of compensation growth, but a reduction in inflation may reduce some of the upward pressure on compensation throughout the remainder of 2023.

Compensation growth could decrease at a more rapid rate due to an external factor, such as a recession. Recessions are generally coupled with higher rates of unemployment, which reduces competition for labor among organizations. Current metrics do not indicate a recession at this time. Specifically, GDP was 1.7% in the first quarter of 2023, and the previous 2 quarters of GDP were 1.2% and 1.9%, respectively, which are all growth states. However, some leading metrics are slowing, which may indicate a weakening of the economy. Specifically, the Bureau of Labor Statistics (BLS) reports that real hourly wages (which account for inflation) have increased by 0.2% over the past year, but weekly hours

have decreased by 0.9% over the same period. The net result is a 0.7% decrease in weekly real wages. Industrial production has also decreased from 3.2% in May 2022 to 0.2% in May 2023, and wholesale sales have decreased by 3.44% YOY as of April 2023.

In summary, there are competing forces between the strong labor market, moderating inflation, and slowing leading growth indictors. A strong labor market and inflation both point toward higher compensation growth, but recent retreats in leading economic indicators indicate some headwinds. ERI expects higher compensation growth continuing in 2023, with the absolute rate of growth slowing throughout the second half of the year. ERI will continue monitoring and reporting on these trends as they unfold over the next several quarters.

Overall Compensation Trends

July salaries have increased by 1.17% (see Table 1) over the April 1 data release. This rate of growth is higher than the predicted quarterly rate of 0.73%. Growth over the past year has been 4.95%, with an average quarterly growth of 1.23%. To put this into context, the average quarterly growth over the past 20 years has been 0.63% (see Table 2). Over the same 20-year period, the average July increase has been 0.60%. Over the past 20 years, July increases (first quarter) have been consistent with increases throughout the rest of the year, and the current quarter is consistent with that trend. The annual growth rate appears to have increased from 4.51% to 4.95%, which is due to July 2022 (0.73%) dropping off the average. Previous quarters growth rates were 1.10% (April 2023), 1.39% (January 2023), and 1.29% (October 2022).

Overall Trends by Year

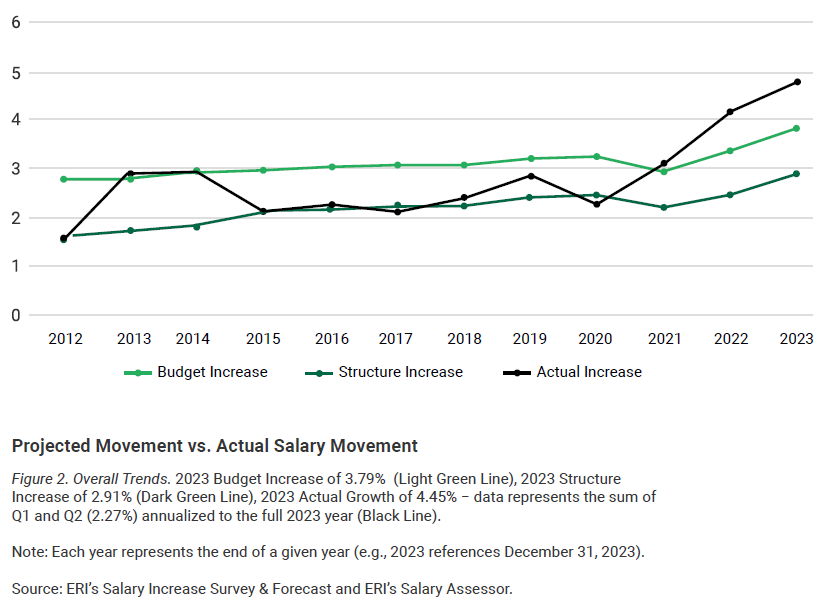

Please refer to Figure 2 below, which has three lines. Two lines (dark green and light green) represent projected salary increases from ERI’s Salary Increase Survey & Forecast, and the black line represents actual changes in salary reported in ERI’s Salary Assessor. The dark green and light green lines represent what survey respondents expected to happen each year (collected in the previous year), and the black line represents what happened in a given year. By comparing these three lines, we can see the extent to which expectations met up with reality. As noted earlier, the actual movement (black line) is expected to follow the structure increase (dark green line). This is because salary surveys generally capture the movement of salary structures within organizations instead of measuring the salary increase of individual employees.

An examination of where the reality of salary movement (black line) has departed from the expected trend line (dark green line) gives us information regarding how salaries might move in the future. Specifically, the past 2013 and 2014 saw actual salaries grow at a rate that is higher than expectations from the previous year. The years 2015 through 2020 were more in line with expected growth (dark green), and growth since 2020 has been higher than predicted.

10-Year Trend by Category

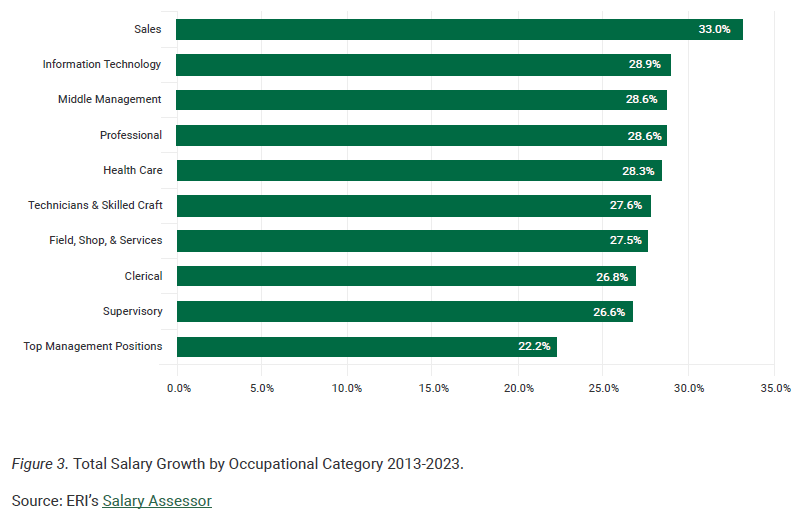

While it is valuable to know how all occupations are moving in this economy, it is also useful to know how different types of occupations move relative to each other and across time. Not all occupations grow at the same rate, and not all occupations grow at the same rate across time. Figure 3 reveals the total growth experienced across a 10-year period. If we break all occupations down into 10 categories, it becomes clear that some occupations are growing at a faster rate than others. Specifically, Sales employees appear to have seen the highest level of growth, whereas Top Management occupations have seen the slowest growth.

Mean Salary by Category

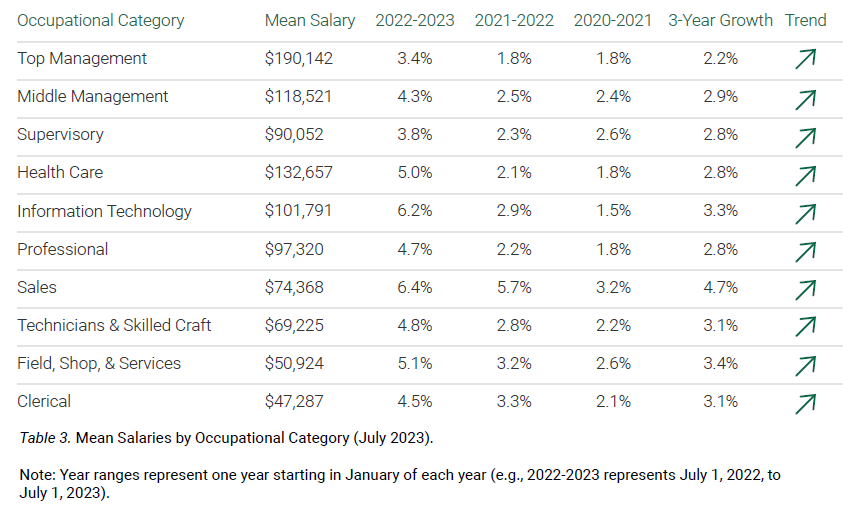

Table 3 reveals the actual growth rates for different occupational categories in the past three years and provides information on whether the occupational category is seeing increased or decreased growth. It is important to note that, just because an occupational category has decelerating growth, it does not mean that the trend will continue. All occupations may be expected

to see salary growth over time, so an occupational category that has been showing slow growth may be more likely to see higher growth in the future.

Occupational Categories

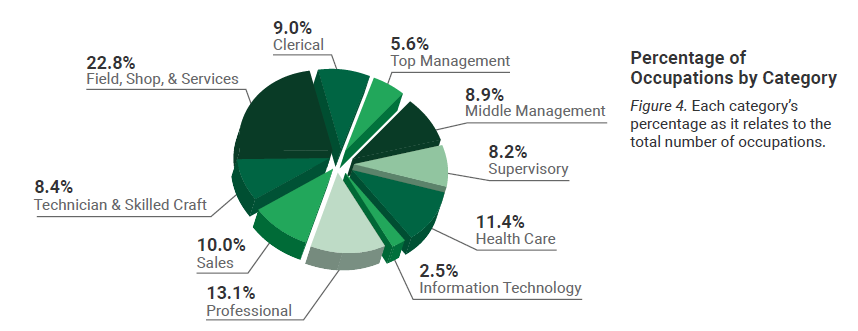

In the process of examining the growth of compensation data on a national basis, the data were broken into ten specific occupational categories to study changes in compensation at a more granular level. The populations of these categories are illustrated in Figure 4 below.

About the National Compensation Forecast

The National Compensation Forecast is designed to capture salary changes across a broad range of jobs found in the United States economy. This index shows how national compensation has changed over the 20 years prior to the time of publication: July 2023. Of note, these figures represent actual and projected salary growth for base compensation only. Other sources include data on the cost of benefits, incentives, and base compensation. By simplifying the analysis and focusing only on the fundamental component of compensation (base compensation), ERI hopes to provide a cleaner picture of how compensation is growing in the United States. The data contained in this report are derived from quarterly results published in ERI’s Salary Assessor, a professional compensation tool used widely across the public and private sector, including most Fortune 500 organizations. For a full discussion of the product’s methodology, please see the Salary Assessor methodology. The specific data used in this report represent 2,052 distinct occupations, which were consistently surveyed across the 20 years covered by this report. These occupations range from the lowest-paid occupation that ERI surveys (Dishwasher) to the highest-paid occupation (CEO) and represent mean base salary. Data are first examined on an aggregate basis before being broken down into 10 occupational categories. The data for the 2023 index comes from data submitted to ERI’s Salary Increase Survey & Forecast.

In coming quarters, ERI will continue to track and report on the trends that exist in the compensation landscape.

Please direct any questions or comments to Jonas Johnson, Ph.D.: [email protected].

By Jonas P. Johnson, Ph.D. and Calvin A. Brooks