All salary negotiations need to begin with research—both employer and employee need to collect meaningful data, not just anecdotes, about typical pay for genuinely comparable positions before beginning compensation discussions. This approach not only makes sense for employers and the executives—it is what the IRS and charity regulators require. See ERI’s Guide to Setting Nonprofit Executive Compensation for a detailed discussion.

For any given job, the level of pay is influenced most by where the job is done—that means (1) the size of the organization; (2) the type of organization; and (3) the geographic location. In the nonprofit sector, the IRS focuses on preventing “excess compensation” and defines “reasonable compensation” as “an amount as would ordinarily be paid for like services by like enterprises under like circumstances.”

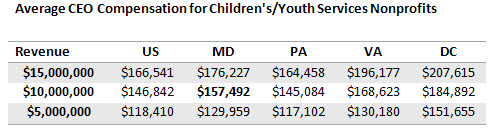

Using ERI’s Nonprofit Comparables Assessor, let’s research what is reasonable compensation for the CEO of a foster care agency in Baltimore, MD, with annual revenues of $10 million. The goal is to find salaries for people who are working in similar organizations with similar responsibilities in order to determine the market rate for the position. The Nonprofit Comparables Assessor database of IRS Form 990 compensation information filed by almost all US nonprofits can be searched selecting the following criteria:

- Job Title: CEO

- Type of Nonprofit Organization: Children’s/Youth Services (where a person with the requisite skills and background and similar responsibilities might be working)

- Location: All US and then a selection of the states of MD, PA, VA, plus the District of Columbia (all places where potential candidates might be working and also places where potential candidates for CEO of a Baltimore-based foster care organization might be employed)

- Size: Annual revenues of between $5 million and $15 million (creating a range around the actual revenues of the organization seeking the market rate for its CEO)

Those criteria are chosen with an eye to the labor market for that CEO position—where would such a person be working with responsibilities for procuring and administering state contracts, recruiting and training foster care parents, dealing with a similar number of staff people, etc.? The idea is to collect compensation for those with similar titles (CEO) in organizations providing similar services (children’s/youth services), and in a similar geographic location (MD and surrounding areas, where the organizations might compete for talent). The search only takes a minute with ERI’s Nonprofit Comparables Assessor and yields the following table.

The table reveals that a reasonable salary for the CEO of this $10 million nonprofit might range from $150,000 to $160,000, but there are many other factors that may enter into determining a final compensation number. Although the national average for the job is lower (around $147,000), the Mid- Atlantic geographic area where potential candidates might come from has a higher average, with the exception of Pennsylvania. To attract someone from DC or VA, the organization might have to pay more, while perhaps someone in PA would be attracted to the job, as average CEO pay in similar organizations is lower there. Other factors that should be considered include the experience level of the candidate or current CEO, the stability and/or growth outlook for the organization (their ability to pay), the compensation philosophy of the organization (some pay top dollar to get the best and the brightest, while others try to find less-experienced or less-qualified people and pay them less). Underpaying people tends to lead to turnover, as the CEO leaves to get the market rate.

Having information on CEO compensation levels in comparable organizations can prepare both the potential employer and the potential CEO for meaningful salary negotiations, in line with the IRS and state charity regulators’ rules and regulations. Using ERI’s Nonprofit Comparables Assessor easily provides that valuable market data.

ERI Economic Research Institute compiles the most robust salary, cost-of-living, and executive compensation survey data available, with current market data for more than 1,000 industry sectors.

ERI’s Assessor Series® – Solutions for every compensation decision