Running a nonprofit arts organization seems to be a challenging job – fundraising, choosing programs that appeal to patrons, expanding the audience, and ensuring that donors and subscribers remain engaged for the long run. How well – or poorly – are these arts organization executives paid?

The category entitled “Arts, Culture, and Humanities” of the National Taxonomy of Exempt Entities (NTEE), the classification system used for nonprofit organizations, comprises only a small proportion of all nonprofits.

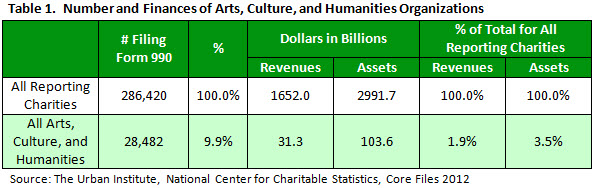

More than one million nonprofit organizations registered with the Internal Revenue Service in the United States are defined as charities (tax-exempt under IRC Section 501c3 and able to receive tax deductible contributions), but only 286,000 of these had enough revenue to require filing a Form 990, the annual IRS information form. Out of the 286,000 reporting public charities, almost 10% were classified as Arts, Culture, and Humanities. The table below also shows how this group represents only a small proportion (less than 2%) of the total revenues in the sector and 3.5% of the total assets in the sector.

These numbers show that there are many smaller organizations in this category, with a larger number of organizations as a proportion of the total representing a smaller proportion of revenues and assets than would be expected. However, a more detailed review reveals the wide disparities in size within this category.

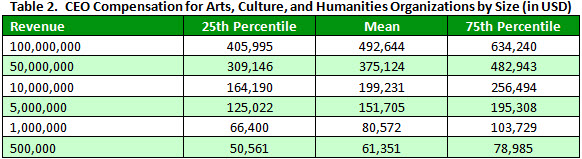

The following examples of compensation for the top job, typically Chief Executive Officer or Executive Director, illustrate the differences in average compensation first by size of organization and then by geographic location.

Using ERI’s Nonprofit Comparables Assessor, average CEO salaries in the United States for all Arts, Culture, and Humanities organizations by size were calculated. Table 2 shows the huge range in salaries paid to CEOs of different-sized organizations.

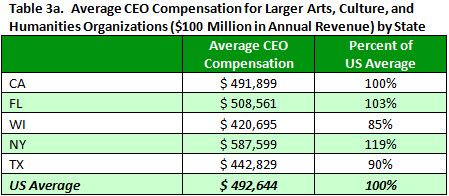

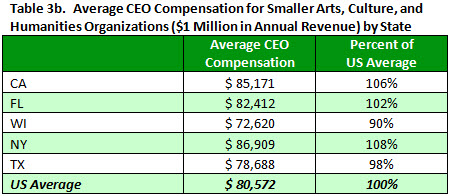

Next, the possible influence of geography on pay was explored. Table 3a lists the compensation for CEOs of larger organizations (with annual revenues of $100,000,000) in several states and the relationship of those average salaries to the US average. Table 3b is a similar table for smaller organizations (with annual revenues of $1,000,000). Again, there is lots of variation in the salaries.

Because the IRS requires that public charities set executive salary levels looking at compensation data from similar organizations (typically defined as similar in type of service or mission, size, and geographic location), it is important to consider a number of the criteria that most influence compensation. The examples in the tables above show that compensation averages by size alone and by geography alone for similarly classified organizations vary widely. ERI’s Nonprofit Comparables Assessor can provide more detailed breakouts to ensure that boards can determine competitive compensation levels for executives that meet IRS regulations.