Last week, the IRS published data on the number of information returns filed by tax-exempt organization in 2012 – 771,675 to be exact – and the number of those returns that were subjected to further examination (meaning the organization was contacted by the IRS for further information, clarification, or a full audit). The number of organizations involved in such an examination of their 2012 returns by the IRS in FY 2013 was 2,882. Most were Forms 990 and 990-EZ (2,744) and the remainder were Forms 990-PF, with a few other forms filed by political organizations and trusts. So, does that low percentage of scrutiny by the IRS mean that nonprofits should have no worries about executive compensation levels?

Not exactly. While nonprofits should comply with IRS rules and regulations concerning executive compensation, others are also reviewing the information. All interested parties can review all Forms 990, as they are public documents posted at several websites including ERI’s Form 990 Library. Of course, the IRS does review the information – its regulatory staff at the Tax Exempt Division holds multiple licenses to ERI’s Nonprofit Comparables Assessor – and is thus able to target its investigations to the organizations that report higher than expected executive compensation when compared to other organizations of similar type, mission, size, and location. So, while data from many organizations may be reviewed to check for “unreasonable” compensation, only those reporting high compensation are selected for further review.

But, states are also reviewing the Form 990 filings and some have even put caps on salaries for nonprofit executives (see States Target Nonprofit Executive Pay for more details). A number of state officials also subscribe to ERI’s Nonprofit Comparables Assessor and use it to evaluate the reasonableness of executive pay. But, the list of interested parties does not stop with regulators at the state and federal levels.

Since many charities are seeking funding from government, foundations, and individual donors, their funding may be jeopardized by an appearance of excessively high salaries. In fact, there are often investigations by the media which trigger further investigation by the government regulators and which may inspire more proposals for legislative action on capping salaries. But even more important, the reputation of paying high salaries to executives can have a devastating impact on donations and funding for nonprofits.

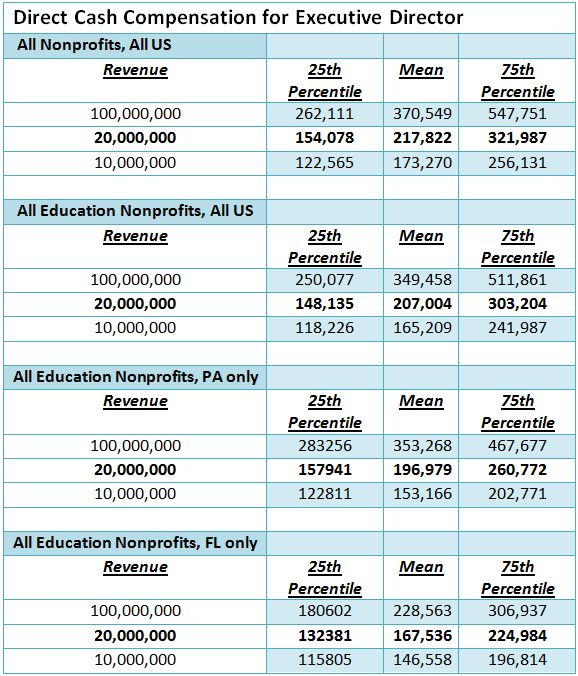

And then there is the basic need to pay the market rate for executive talent – if too little is paid, retention and motivation will be problems; if too much is paid, there will be criticism and perhaps less money available to fund the mission of the organization. Finding that market rate isn’t as simple as finding a general average from a national survey. Setting market rates requires using criteria such as type of organization, size, and location to get it right. The table below, created using ERI’s Nonprofit Comparables Assessor, highlights the need to use specific criteria to develop appropriate compensation levels. For example, average executive director compensation for all types of nonprofit organizations with $20 million in annual revenues in the US is very different from compensation for the same position in an education organization in Pennsylvania or Florida.

So, the type of organization, the size, and the location all make a difference in determining appropriate and defensible compensation levels. ERI’s Nonprofit Comparables Assessor allows the selection of comparable organizations using the relevant criteria, so that compensation reflects the labor market for the executive and is defensible to all stakeholders.