Massachusetts Attorney General Martha Coakley released a December report on nonprofit executive compensation highlighting some high salaries, particularly in the health and education fields (see http://www.mass.gov/ago/docs/nonprofit/ceocomp/ec-review.pdf for the complete report).

The report states, “While CEOs at for-profit companies have commanded the highest compensation packages, CEO compensation at public charities has also increased. In fact, high executive compensation at public charities frequently leads to greater levels of concern, because of the view that large compensation packages take money away from charitable missions. They can also negatively affect the perception of the charities with employees, donors and other constituencies, as well as with the general public. At the same time, the largest public charities are complex organizations in their own right, and demand a level of executive ability that is at least commensurate with that complexity.”

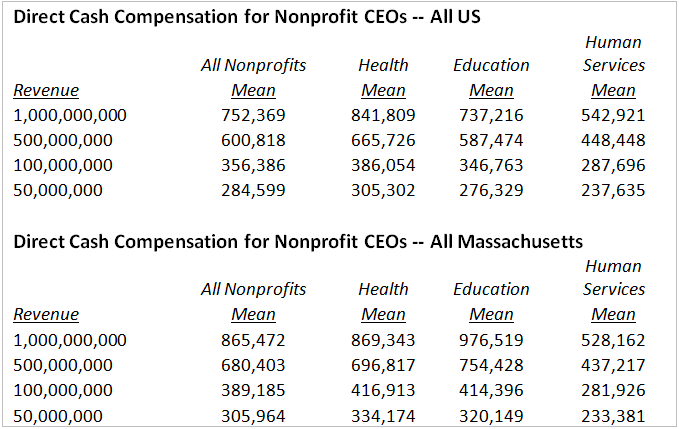

ERI’s Nonprofit Comparables Assessor was used to see how different types of Massachusetts nonprofit CEOs fared in direct cash compensation when compared to their counterparts in the entire United States.

In general, there are significant differences in compensation levels among the different types of large nonprofits (health, education, and human services) in the all US and Massachusetts comparisons shown above. Compensation in human services organizations is consistently lower. Also, at the larger revenue levels, health organizations tend to pay more across the US, while, in Massachusetts, the largest education organizations pay more.

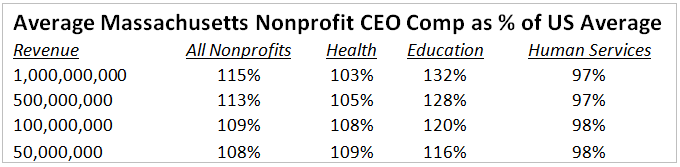

So how do the Massachusetts salaries compare with the US averages? The following table illustrates that, while human services organizations tend to pay less in Massachusetts, both health and education organizations pay higher than the US average (particularly in education).

The AG’s report states that “the organizations in our study approached setting the CEO’s compensation with care and attention to the standards the IRS has set forth creating a presumption that the compensation is reasonable. Despite the care these organizations took in setting CEO compensation, we found little evidence that the process restrained CEO compensation or its growth.” However, it must be noted that the purpose of the IRS regulations on compensation is to assure comparability, and the focus is on using data from similar organizations to set salaries. The purpose is not to restrain CEO compensation but to determine market levels.

How this report will be used in Massachusetts is not yet clear, but, until there are regulatory or legislative changes, all nonprofit organizations should be collecting compensation data from similar organizations to assist in the setting of executive compensation. ERI’s Nonprofit Comparables Assessor provides easy access to that information, allowing the user to choose the relevant type, size, and location of the comparable organizations.