Boards of nonprofits are tasked with setting compensation for their executives, and there are some compelling reasons to do it right.

#1 – IRS Review

Federal tax law prohibits individuals who control or have a close relationship with nonprofit organizations from benefiting unfairly from the entity’s assets. The IRS will be reviewing the compensation for executives, as the organizations must file a Form 990 each year that includes that data. (Note that, in some states, there will also be a review by state charity regulators.)

#2 – Public Scrutiny

Forms 990 are public information, available by law from the organization and posted on several web sites. This means that potential funders (e.g., governments and private foundations) and individual donors can easily review salary levels, as well as the media, and even users of the services nonprofits are providing. Salaries that look excessive may be a problem for those looking to support a charity or use its services.

#3 – Proper Use of Charitable Funds

Board members have a fiduciary responsibility to use charitable funds properly – paying salaries that are not supported with comparable data, as required by IRS regulations, does not meet that test. If the Board has based pay decisions on compensation paid to executives providing “like services by like enterprises under like circumstances” according to Form 990 instructions, then the Board has exercised appropriate care in allocating charitable resources.

Making the “Right” Decision on Pay

Nonprofit executives (and key employees) should receive “reasonable compensation,” which the IRS does not define precisely, leaving the term open to a wide variety of interpretations. As a result, the IRS reviews executive compensation – and penalizes – tax-exempt organizations that excessively reward their leaders.

Some organizations, like the National Football League, have actually relinquished tax-exempt status, at least partially because of negative attention to top executive pay in a “nonprofit.” Learn more about that change to for-profit status in my 2015 blog post.

While the IRS does not define “excessive compensation,” there are guidelines for determining executive compensation, and the IRS actually seems more interested in knowing the process used, as it views increased transparency as a way to limit excess compensation. The IRS wants boards to collect and use data from comparable organizations to set salaries, so the crucial step is to determine which organizations are comparable. According to the IRS, this data are most likely relevant if from organizations that fulfill these criteria:

- Similar in purpose, service provided, or activity. For example, day care providers should be compared with other day care providers and hospitals with other hospitals. The IRS uses the National Taxonomy of Exempt Entities (NTEE) code to categorize all types of nonprofits, so using these codes helps identify similar entities. Find more information at http://nccs.urban.org/classification/national-taxonomy-exempt-entities.

- Similar in size. This is typically measured using annual revenues listed on the Form 990. For some types of nonprofits, such as credit unions or foundations, the most appropriate measure of size might be assets, rather than revenues.

- Similar in geographic location. This may or may not be used depending on the labor market for the position of interest. If executives qualify and compete for this job in the local area (e.g., the executive director of a day care provider), then the local region should be searched for comparable organizations. However, if this is a large national organization (e.g., a large hospital), then the search for a successor would include major cities or all 50 US states; in this case, the search for comparable entities should be expanded to a larger area.

Once comparable organizations are found, the next research step is the job match – for example, do the Chief Operating Officers in the comparable organizations actually have similar job duties and responsibilities to the COO in the organization of interest? Are similar education levels and similar credentials/licenses, if any, required?

If these criteria are met, then data on compensation will probably be deemed relevant by IRS. However, the board is permitted to take other factors into account when the final compensation is set. The IRS is most interested in making sure that the process of collecting comparable data was completed and that the data were used in the discussion of compensation levels. Of course, Board members should document compensation decisions and know that they can support their decisions with data.

Some Examples

ERI’s Nonprofit Comparables Assessor software provides an easy way to find comparable organizations and compensation data. Here are two examples:

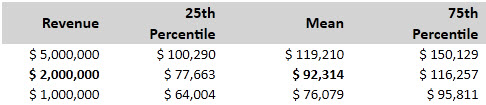

Example: Small Day Care Center, located in Akron, Ohio

NTEE: Youth Development Organizations

Size: Annual revenues of $2 million (range of $1-5 million)

Geographic Location: Akron, Ohio (state-wide labor market)

Job Title: Executive Director

The data show that, in the state of Ohio, an Executive Director of similarly-sized youth development nonprofits is typically paid between $78,000 and $116,000, with an average of about $92,000. The Nonprofit Comparables Assessor also provides a list of the organizations that meet the criteria so that the most relevant can be selected for further analysis, ensuring comparability of the data.

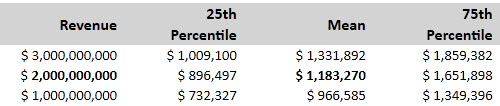

Example: Large Hospital, located in Chicago, Illinois

NTEE: Hospitals

Size: Annual revenues of $2 billion (range of $1-3 billion)

Geographic Location: Chicago, Illinois (US-wide labor market)

Job Title: CEO

Most CEOs in similar hospitals across the US typically earn between $897,000 and $1,652,000, with an average of about $1,183,000. A more detailed look at the data will reveal which hospitals provide the most relevant comparisons for the salary decisions.

While these averages can give the board members some boundaries and a context for compensation levels, more detailed review and discussion of all factors is needed to finalize compensation decisions.