Boards setting nonprofit CEO compensation have a lot to consider – they need to set salaries that attract and retain the leaders needed by the charity and also fulfill their fiduciary responsibilities to allocate the charity money wisely. At the same time, they must be compliant with IRS regulations on “reasonable compensation” (and perhaps state regulations) with an awareness of the potential for public scrutiny.

Research on compensation concludes that, for any given job, the level of pay is influenced most by “where” the job is done – and “where” most often means (1) the size of the organization; (2) the type of organization; and (3) the geographic location.

In the nonprofit sector, the IRS focuses on preventing “excess compensation” and defines “reasonable compensation” as “an amount as would ordinarily be paid for like services by like enterprises under like circumstances.” This again is the concept voiced by compensation professionals in all sectors — pay is based on what you do and where you do it. The IRS clearly wants nonprofits to consider the influence of organizational characteristics when collecting comparative data for a given job.

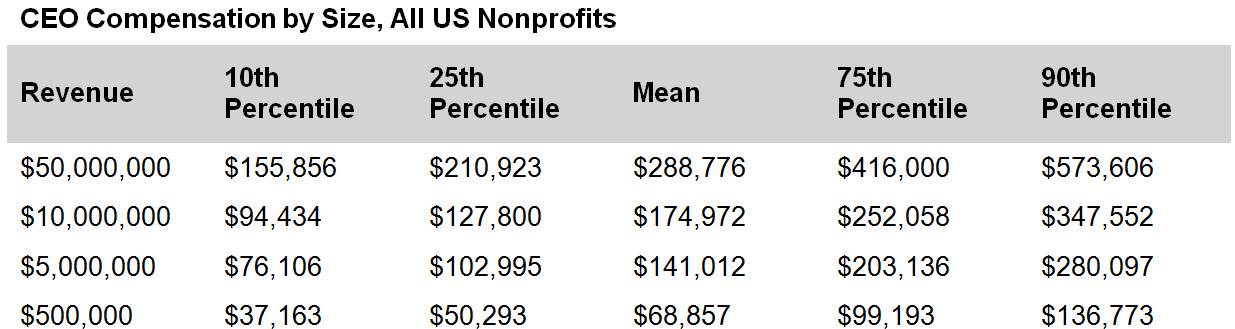

Size of Organization

Using ERI’s Nonprofit Comparables Assessor, the table below was created to illustrate the impact of size on compensation. Compensation ranges for the CEO of a human services organization of varying sizes (as defined by annual revenues reported on the Forms 990) are shown.

This illustrates how the size of annual revenues affects salary levels. So, should the human services organization with annual revenues of $10 million pay its CEO about $175,000? Not so fast.

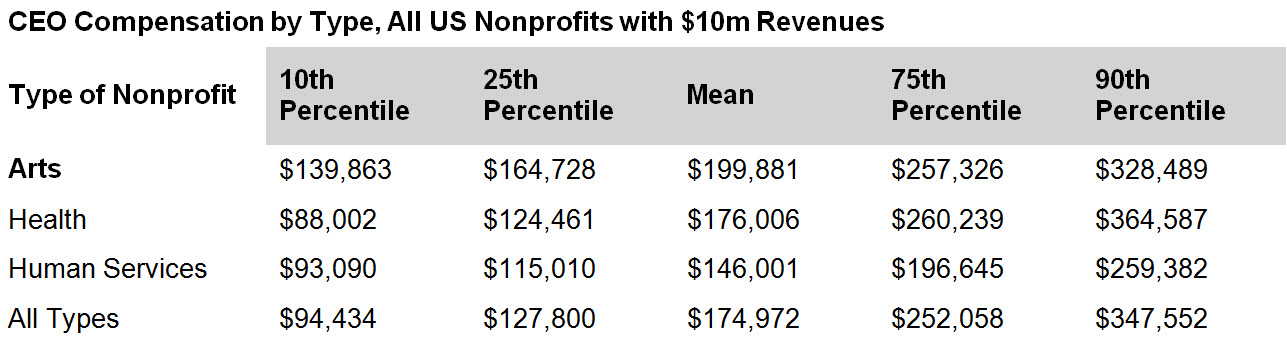

Type of Organization

The next factor to analyze is the influence of the types of organization – what services are provided in what field? Organizations of similar size, using $10 million for this example, reveal wide differences in pay. This analysis, based on compensation reported by nonprofits on their annual Form 990 returns filed with the IRS, is easily generated by ERI’s Nonprofit Comparables Assessor.

This seems to indicate that the CEO of the $10 million human services organization should be paid around $146,000, rather than $175,000. But, at least one more factor should be reviewed.

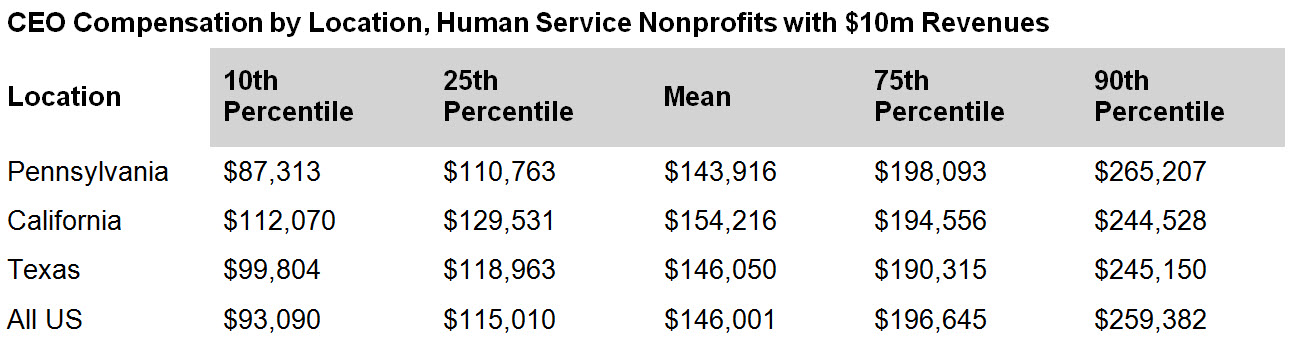

Geographic Location of Organization

What other similar organizations (human services with annual revenues of $10 million) are paying their CEOs in different geographic locations also should be reviewed.

So, the location of the $10 million human services organization is also important in setting salaries. As shown above, this CEO would expect an annual salary of around $144,000 if the organization was in Pennsylvania, versus $154,000 if the job was in California.

Other Considerations

In addition to the major influences on compensation shown above, there are some other factors that might need consideration:

- Other comparable organizations from other sectors. While nonprofit data may be the most likely source of comparable information, salary information from government or even for-profit companies could be relevant for certain positions, where a candidate might have or need experience from other sectors.

- Salary relationships within the organization. Setting a salary using other outside organizations may require adjustments to salaries for other positions within the organization. The spread between the CEO salary and the salaries of other employees may be important to recruiting and keeping a qualified committed workforce.

- Budget constraints. The Board members setting the salaries are responsible for the budget for the organization (including the CEO salary), so salary increases must be planned in a manner not to cause financial stress.

While IRS Instructions for the Form 990 will give the requirements (page 68 covers “reasonable compensation”), there is a lot more to determining nonprofit compensation that is not too high and not too low. ERI’s Nonprofit Comparables Assessor easily provides the compensation data from comparable organizations that can help in that decision.