While there are some situations that call for standing out from the crowd, setting nonprofit executive compensation is not one of them – that is, unless there is a thoughtful process that is not only supported by data, but also well-documented, and justifies a higher-than-expected salary.

The IRS is looking for outliers when it investigates compensation for nonprofit executives. When nonprofit executive salaries are at the higher end of the range for similar nonprofits, it becomes very important to take all the necessary steps to document that compensation is reasonable. The IRS looks at compensation data reported on Forms 990 and so should those who are responsible for determining what compensation should be in their organization.

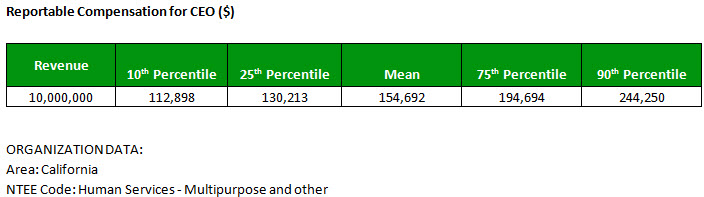

An easy first step to see if a particular executive salary is an outlier is to use ERI’s Nonprofit Comparables Assessor (CA), actually the same software that is used by IRS investigators. The IRS wants data for “similar organizations” to be used in the comparison, so the CA software uses the Form 990 data from organizations with similar characteristics to calculate an average salary. “Similar” organizations are defined based on criteria chosen by the user – for example, similar in type and services provided (the National Taxonomy of Exempt Entities code); similar in size (annual revenues reported on Form 990); and similar in geographic location (all US, one state, or selected states). The table below, generated by ERI’s Nonprofit Comparables Assessor, shows the expected direct compensation for the CEO of a mid-sized Human Services organization in California, based on data reported in the Forms 990 of organizations meeting the selection criteria.

So if the CEO in question is paid less than or around $155,000, then the organization can feel pretty comfortable that there will be few questions about reasonable compensation from regulators, charity watch groups, clients, funders, etc. However, if the pay is much higher, say more than $195,000, additional data are needed for documentation that will be available to respond to possible questions about salary levels.

The next step is collecting more detailed data on perhaps 10 to 15 organizations that are most similar – the organizations that may be those providing similar services that have CEOs with similar backgrounds and experience. Again ERI’s CA can easily provide a list of all organizations that meet the selected criteria, and then the user can select the closest in size, geography, and mission name. The list also includes a link to the Form 990 of each organization so that the most recent form can be accessed and a detailed review of the purpose and compensation can be completed. The table below from ERI’s Nonprofit Comparables Assessor shows four of a larger list of similar-sized Human Services organizations with revenues of $10-11 million in California, reflecting a range of salaries.

From a list of all organizations that meet the criteria selected, more directly comparable organizations can be chosen for a closer look. This could include a more precise type of Human Services organization, such as those providing after-school care versus literacy programs, or a more narrow range of revenue size, such as $9-12 million, or a smaller geographic area, such as the San Francisco Bay area versus the state of California. The four organizations above pay their CEOs very different amounts, so it is crucial to be able to show which ones are most similar to determine what is reasonable for compensation.

Current regulations – federal and state – do not prevent an organization from paying on the higher end of the salary range for similar positions in similar organizations. In fact, higher total compensation can be reasonable given an employee’s experience and expertise, plus any special circumstances. What paying at a higher level does require is data that support such compensation as fair and reasonable.

Compensation decisions must be thoughtful and backed up with data. ERI’s Nonprofit Comparables Assessor provides easy access to the same Form 990 compensation data that regulators are using to locate outliers. If nonprofit executive pay is above what might be expected, then it is important to collect, analyze, and make decisions based on the data.