So right along with the coming holidays, thoughts of bonuses and salary increases begin to surface this time of the year. Contributing to this discussion is the publication of various annual reports on last year’s average compensation increases and plans for 2016. USA Today reports on one study that found that employee bonus pools are below target and will be funded less than last year, while another concluded bonus pools are on target.

There is agreement on one compensation basic – raises in base pay are rare and getting more so. This is part of the long-term trend by employers to move to a variable compensation concept, reducing the proportion of pay that is “fixed” (i.e., the base) and increasing the proportion that is “variable” (i.e., bonuses that are not built into the base and vary from year to year). Although nonprofits often have uncertain revenues, frequently beyond their control, some have tried to emulate for-profit companies and increase the use of bonuses also.

How valuable is information on average increases to those responsible for setting wages? Better questions are “Is turnover increasing?” and “Can we attract and retain the talent we need to our organization?”

In the nonprofit sector, GuideStar’s annual study of executive compensation in the nonprofit sector gives a broad view of increases for past CEOs, using Form 990 data from over 90,000 organizations, with these findings:

- The median pay increase for top executives at nonprofits was 2.2% in 2012, up from 2% in 2011 and 1.6% in 2010.

- Median salaries for arts, religion, and animal-related organizations were the lowest, while health and science were the highest.

- The Washington, DC, area had the highest overall median salaries, while compensation in the Atlanta, GA, area was the lowest.

- CEOs in large charities had median increases of about 4% in 2012 (median salary of $444,108), while increases for charities with less than $250,000 were about 1% (median salary of $44,806).

So what is the “right” increase for 2016? What you do (i.e., the job) and where you do it (i.e., type, size, and sometimes location of organization) are still most important. The data needed for comparison must be collected from similar organizations, and what is important is the salary actually paid, not the rate of increase. What must be considered is how the current pay aligns with salaries in comparable organizations. Overall averages and medians always seem to be of great interest but are a poor basis to determine market rates that follow IRS criteria.

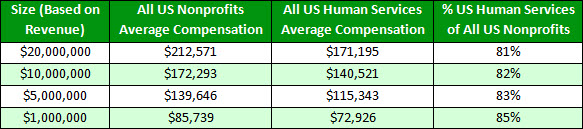

For example, Table 1, created using ERI’s Nonprofit Comparables Assessor, shows how applying average increases to a salary to come up with CEO compensation can lead to trouble – and may fail to meet the IRS requirements for setting nonprofit executive salaries. There is a definite difference in pay among different sizes of nonprofit organizations (even in the relatively small sizes shown below), but there is also a variation in pay for different types of nonprofit organizations, illustrated using average salaries for all Human Services CEOs compared with those for all nonprofits.

Table 1 — Comparison of US Average CEO Compensation for All Nonprofits and Human Services

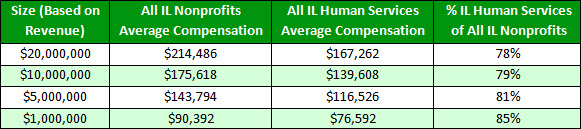

If the organization of interest provided human services in Illinois and had annual revenues of about $10 million, an average can be calculated that includes only organizations that are comparables, as shown in Table 2. Again, it is clear that the type of organization and its size are important when determining market salary levels, but geographic location should also be considered.

Table 2 — Comparison of Illinois Average CEO Compensation for All Nonprofits and Human Services

The only way to assess appropriate compensation levels is to use data from comparable organizations, similar in type and size, and perhaps in geographic location. Although this requires much more data collection than a review of general surveys, it is easily accomplished using ERI’s Nonprofit Comparables Assessor. Nonprofit boards will then be assured that their CEO compensation is competitive and their process is in compliance with IRS standards.