Before addressing either the obvious question, “Does crime pay?” or, more precisely, “What do the CEOs of crime and legal-related nonprofits earn?” let’s take a look at how this type of organization fits within the nonprofit sector in the US. The National Taxonomy of Exempt Entities, the classification system used in nonprofit research and in ERI’s Nonprofit Comparables Assessor, includes Crime and Legal-Related organizations (Major Group I) as a part of the broader division of Human Services organizations. More specifically, Major Group I consists of organizations addressing and influencing policy and providing services in areas such as these:

- Crime prevention, including drunk driving and delinquency;

- Correctional facilities, such as half-way houses for offenders/ex-offenders;

- Rehabilitation services for offenders and their families, plus prison alternatives;

- Court reform and alternatives to litigation and sentencing, such as dispute resolution and mediation services;

- Protection against and prevention of neglect, abuse, and exploitation; and

- Legal services, including public interest law and litigation.

According to the Internal Revenue Service statistics, [i] close to one million nonprofit organizations are registered with the Internal Revenue Service in the United States, but only 37% of them have revenues that reach the level of $50,000, which requires the filing of an annual Form 990 (with the exception that all private foundations of any revenue or asset size must file a Form 990-PF).

Of the over 350,000 reporting tax-exempt organizations (meeting the revenue requirement for filing a Form 990), about 34% are involved in providing what is defined by the NTEE as human services. Although Human Services is by far the largest type of reporting nonprofits, Crime and Legal-Related organizations comprise only 5% of Human Services and less than 2% of all nonprofits. The table below shows how this major group compares in annual revenues and assets to the rest of the nonprofit sector.

Table 1. Number and Finances of Crime/Legal-Related Organizations, 2014

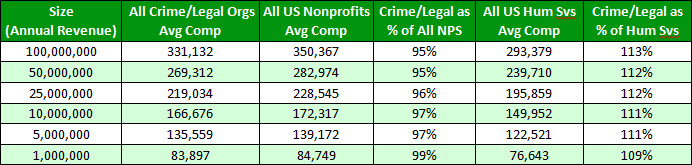

ERI’s Nonprofit Comparables Assessor can be used to analyze average CEO salaries by size and type of nonprofit organization. The table below compares compensation of all nonprofits, all Human Services, and Crime/Legal-Related organizations.

Table 2. CEO Compensation for Crime/Legal-Related Organizations by Type and Size

Human Service organizations have lower average CEO compensation compared to all US nonprofits for all revenue levels shown above. However, the averages for Crime/Legal-Related organizations (included in total Human Services) reveal a different finding. The average compensation for CEOs in Crime/Legal-Related organizations at all sizes is less than the average in all US nonprofits, but it is greater at all sizes when compared to all Human Services. So crime, in fact, does pay, at least when compared to other Human Services organizations (just not when compared to all nonprofits).

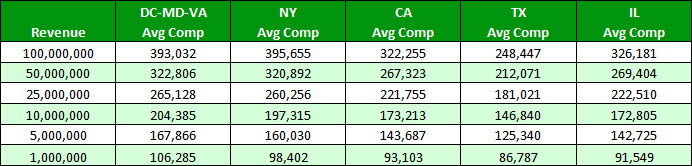

Another factor that typically influences salary levels is geographic location. The compensation averages for CEOs from the Nonprofit Comparables Assessor show significant differences among different states. Since many of the nonprofits working to influence national policy are located near Washington, DC (including DC itself, suburban Maryland, and northern Virginia), the compensation data for organizations in this area are combined and shown as DC-MD-VA. Indeed, salaries seem to be higher for organizations in this area that tend to focus on national policies relating to crime and the legal system, particularly for the largest nonprofits.

Table 3. CEO Compensation for Crime/Legal-Related Organizations by State and Size

The IRS requires that public charities set executive salary levels by looking at compensation data from similar organizations (typically defined as similar in type of service provided, size, and geographic location). There is clearly a need for detailed comparisons using relevant data to ensure that compensation levels comply with IRS regulations.

[i] Internal Revenue Service, Exempt Organizations Master File (2014, June)